Well, it’s options expiration week again and as usual Wall Street is gunning the market for all it’s worth. The bulls are falling for this shenanigan yet again, just as they did in June.

How’d that work out?

Tracking options week manipulations isn’t easy because there are no strict rules: the action all depends on where the market is and the number of outstanding contracts at given price points.

For instance, back in April investor bullishness was at extremes. Consequently, Wall Street ramped stocks first upwards (the usual predilection) to shank the puts… only to swiftly reverse the action in the middle of the week to shake out the calls.

This whole system occurs courtesy of the Federal Reserve which openly and blatantly pumps the market on options expiration week. I’ve shown the below chart before. It’s staggering that no one in Congress or any of the regulators actually bother following up on this. How much more obvious does Bernanke need to get?

Options expiration weeks in bold

Week

Fed Action

July 8 2010

+$1 billion

July 1 2010

-$13 billion

June 24 2010

+$175 million

June 17 2010

+$12 billion

June 10 2010

-$4 billion

June 3 2010

+$2 billion

May 27 2010

-$16 billion

May 20 2010

+$14 billion

May 13 2010

+$10 billion

May 6 2010

-$4 billion

April 29 2010

-$1 billion

April 15 2010

+$31 billion

April 8 2010

+$420 million

April 1 2010

-$6 billion

March 25 2010

+$5 billion

March 17 2010

+$25 billion

March 11 2010

+$2 billion

March 4 2010

-$5 billion

February 25 2010

+$8 billion

February 18 2010

+$21 billion

February 11 2010

+$7 billion

February 4 2010

+2 billion

January 28 2010

-$4 billion

January 21 2010

-$39 billion

January 14 2010

+$56 billion

January 7 2010

+$1 billion

December 31 2009

-$1 billion

December 28 2009

+$35 million

December 17 2009

+$49 billion

December 10 2009

-$17 billion

December 3 2009

-$2 billion

November 27 2009

-$2 billion

November 19 2009

+$73 billion

November 12 2009

-$30 billion

November 5 2009

+$3 billion

October 29 2009

-$39 billion

October 22 2009

+$8 billion

October 15 2009

+$54 billion

October 8 2009

-$3 billion

October 1 2009

-$17 billion

September 24 2009

+$18 billion

September 17 2009

+$51 billion

September 10 2009

+$4 billion

September 3 2009

+$8 billion

August 27 2009

+$14 billion

August 20 2009

+$46 billion

August 13 2009

+$25 billion

August 6 2009

-$11 billion

July 30 2009

-$38 billion

July 23 2009

-$33 billion

July 16 2009

+$80 billion

Notice that on non-expiration weeks the Fed either pumps the system slightly or, more commonly, removes money.

However, once options expiration week hits, it’s PUMP time. To whit, the Fed has NOT had a single options expiration week in which it HASN’T pumped the market in nearly one year.

Moreover, note that despite the Fed’s Quantitative Easing Program ending in March, the Fed continues to pump $10+ billion into the system EVERY month when options expiration week rolls around.

Didn’t Bernanke say he wouldn’t continue buying assets from Wall Street after QE ended? More importantly, didn’t QE end? Why is the Fed still pumping money into this system?

And finally… how many times does this have to happen before someone in power actually notices it? Seriously, we’re talking about the Fed going 12 for 12 in the last year. And it’s not like the pump jobs are even subtle: they’re DRAMATICALLY larger that any other capital infusions the Fed makes during non-options expiration weeks.

Good Investing!

Graham Summers

PS. For more hard-hitting investment insights revealing the real reasons the market moves as it does, join me at www.gainspainscapital.com

Congress is in a fierce debate over whether — or how — to extend the Bush administration tax cuts. How does that affect you? The Tax Foundation has come up with a new tax calculator that allows people to figure out their 2011 tax burden under three scenarios:

(1) Congress allows all of the Bush tax cuts to expire.

(2) Congress extends into 2011 all of the Bush tax cuts.

(3) Congress passes the tax laws proposed in President Obama’s budget, letting some tax cuts expire, extending some, and enacting some new tax laws.

Be prepared before you use the calculator as it is is fairly complicated, with 19 inputs from income to the number of dependents and dividend income.

Thanks! now what is $8,000 divided by $180,000

-ummmm 4.4% repeating

Wow look at that! people selling their houses knew that the people buying were going to receive $8,000 and they raised the price of their house an average of $8,000. What a great deal for new home buyers using the tax credit!!!

Marc Faber closed out this week's Agora Financial Symposium with a speech that pretty much recapitulated the view that the end of the world is if not nigh, then surely tremendous dislocations to the existing socio-political and economic landscape are about to take place (with some very dire consequences for the US). His conclusive remarks pretty much summarize his sentiment best: "We've had a trend for most of the past 200 years: GDP of countries like China and India went down while the West surged. That's now changed.

Emerging economies will go up, and your children in the West will have a lower standard of living than you did. Absolutely. We won't sink to the bottom of the sea. But other countries will grow much faster than us. The world is very competitive, and the odds are stacked against us. Americans, with their inborn arrogance, will not let it go that easily, so there will be lots of tension going forward." While long-time fans of Faber will not be surprised by the gloom and doom (not much boom) here, anyone else who still holds a glimmer of hope that at the end of the day the CNBC spin may be right, is advised to steer clear of Faber's most recent thoughts.

And while we do not have the full presentation yet, the salient points have been recreated below courtesy of the Motley Fool. For those who desire a far more in depth presentation from the inimitable Mr. Faber, we direct you to his June 2008 capstone presentation: "Where is the boom, and the doom" - link here.

On reality: My views are not all that negative. I think they're just realistic. I want to face reality. You have people like Paul Krugman who thinks we should have another bubble to pull us out of this. He actually said that. But he said the same thing in 2001. And you know how that turned out.

On unintended consequences: The Fed doesn't seem to have learned anything at all from its mistakes. Their current policy of cutting rates to zero is designed to create sustainable growth, but they've created larger and larger volatility in markets. There are many unintended consequences of their actions.

The oil bubble of 2008 is a good example. In 2008, the price of oil went ballistic, but the U.S. was already in a recession [it began in Dec. 2007]. There was no rational reason oil should have gone ballistic. The Fed's easy money just fueled a bubble. It was like a $500 billion tax on consumers courtesy of the Fed. That's the added amount that it cost you, and it helped push consumers over a cliff in late 2008.

On the Fed: The Fed doesn't pay any attention to asset bubbles when they grow. That's their official policy. But they flood the system with cash when bubbles burst. They only care about bubbles when they crash. It's a very asymmetric response and it has many unintended consequences.

Letting bubbles inflate and then fighting them when they burst actually worked for a while. That's what makes it dangerous. It worked in the '90s. But you shouldn't read too much into this: This period was assisted by unusually favorable conditions. From 1981 until early last decade, commodities were in a bear market after a bubble in the '70s and early '80s. And interest rates were falling throughout the '80s and '90s, too. They almost never stopped falling. That made Fed policy look like it was working.

Bubbles can still happen without expansionary monetary policy. In the 19th century, you had bubbles in railroads, for example. But today, the Fed has created a bubble in everything -- in every single asset class. This is an achievement even for a central bank. Stocks. Commodities. Bonds. Real estate. Gold. Everything goes up when the Fed prints. The only asset that goes down is the U.S. dollar.

On deflation: I'm a believer that the stock market lows of March 2009 will not be revisited. You have people like Robert Prechter who think the Dow will collapse to 700 because of debt deleveraging. Debt deleveraging could happen, but the Dow will not fall because of monetary policy. The Fed will keep everything inflated in nominal terms. And if the Dow does go to 700, you'll have more to worry about than your investments. All the banks will be bust. The government will be bust. You don't want cash if massive deflation happens. On the contrary: It will be worthless. You have to think very carefully about hardcore deflation.

On credit addiction: In a credit-addicted economy, you don't need credit to actually fall for there to be problems. All you need is a slowdown in the growth rate, and you get big problems. Now, the government and the Fed are aware of this, so they are creating debt through fiscal deficits and monetization. That creates a hugely volatile environment. In 2008, government credit creation was inferior to private credit contraction, and asset markets tanked. In 2009, government credit creation was higher than private contraction, and asset markets went ballistic. Lately, government credit creation has slowed, and asset markets have gone down. Now, the Fed is aware of this, and it's only a matter of time before it throws more money into the system. I guarantee this.

On what the Fed will do from here on out: The easiest way to fix our debt problems is with 6% inflation per year. That bails out everyone in debt. Interest rates will stay at 0% in real terms forever, in my opinion. If inflation is 5% per year, the Fed will keep interest rates at 5%; that's how you get 0% real interest rates. Now, we could have debt contraction in the private sector, but it doesn't matter. It will be more than an offset with government debt creation. So it's not a good idea to be all in cash and out of stocks. Cash is very dangerous when central banks want real interest rates at 0%.

On the rest of the world: The U.S. today is much worse off than it was 10 or 20 years ago compared with the rest of the world. The Asians should thank the Federal Reserve for this. The Fed practically created the emerging market economies. The Chinese pegged its currency to the dollar in 1994, and until 1998 not much happened. When the Fed began printing and boosting asset prices in 1998, there was this huge debt growth, and U.S. consumers began spending at a massive rate. That increased our trade deficit from $200 billion to $800 billion. Of course, trade deficits have to be offset by trade surpluses in other countries. So the Chinese began ratcheting up production. Then their employment went up. Their wages went up. Entrepreneurs began investing more money in capital spending. The Fed is not the only factor that led to strong emerging market growth, but it certainly was a major factor in it.

On delusions of grandeur: In the U.S., we still think that we are the largest consumer market in the world. For some services we are, but in general this is the wrong way to look at things.

There are huge differences in how statistics between countries are produced. For one, the U.S. is the most leveraged. Other countries factor this in. Also, consumption in the U.S. is 70% of GDP, but it's almost all on domestic services. Spending on actual goods is only 20% of consumption. In the U.S., we spend $600 billion a year on defense. But $300 billion of this goes to personnel and retiree costs. In China, the cost of personnel is basically nothing. When you adjust for purchasing power, China probably spends about what the U.S. does on military capital.

We also think that we have all the knowledge of the world. We think that's our edge. But knowledge in countries with much larger populations have the edge. Research now is being done in Asia because it's cheaper there. Companies like Intel, IBM, and Microsoft are researching in Asia. It's just so much cheaper there. And they are smarter than the U.S. in many ways, too.

Facing dangerously low approval ratings for an incumbent, Senate Majority Leader Harry Reid has turned to an age-old tactic in his bid for re-election: scaring senior citizens.

As soon as Sharron Angle emerged as his Republican opponent, Reid made Angle’s professed support for personal retirement accounts a centerpiece of his campaign against her, launching a series of ads blasting her for wanting to “wipe out” Social Security.

Reid’s gambit to defend his seat in a state with the nation’s highest unemployment rate is part of a broader effort by Democrats to navigate a difficult electoral environment. With a weak economy and a public that has turned against President Obama and his agenda, Reid and his fellow Democratic incumbents are trying to resurrect their glory days, when they were the only ones standing in the way of President Bush’s sinister plot to destroy the popular but fiscally unsound government program.

The strategy was telegraphed in late January, when Obama cited Rep. Paul Ryan’s “Roadmap for America's Future” entitlement reform plan in his talk at the House Republican retreat as a “serious proposal” that he nonetheless opposed. Soon after, the Democratic National Committee pounced on the plan and leading Democrats argued that because Ryan was the ranking GOP member on the Budget Committee, it showed that Republicans wanted to “privatize” Social Security.

The weak-kneed Republican leadership has mostly distanced themselves from Ryan’s ambitious plan, emphasizing that it wasn’t the official Republican budget. And in the midst of campaign season, any GOP candidate who has indicated support for Ryan’s proposal has been subjected to relentless attacks.

In the race for Wisconsin’s 7th Congressional seat, for instance, Democrat Julie Lassa has blasted Republican Sean Duffy for making general statements in support of Ryan’s plan, which calls for voluntary personal accounts for younger workers and other changes to make the Social Security system solvent.

The campaign season debate over Social Security is set against the backdrop of Obama’s fiscal commission. While conservatives are convinced that the body is just a Trojan Horse for a European style value added tax, liberal activists are worried that it’s part of a plan to cut Social Security.

Last Wednesday, the liberal group MoveOn.org sent out an email seeking to raise $185,000 to launch a preemptive campaign against any efforts to cut Social Security. The ominous email warned of a “showdown coming to Washington” over Social Security, with conservatives and Blue Dog Democrats on one side, and “progressives” on the other. As of this writing MoveOn had raised $192,489, and had set a new goal of $250,000.

As part of the effort to avert any serious attempts to do something about the looming Social Security crisis, liberals have sought to deny any crisis exists in the first place.

Nancy Altman, co-director of the group Social Security Works, a coalition of unions and other liberal activist organizations, argued that “Deficit hawks plotting to cut Social Security to reduce the deficit are seriously misguided. The truth is that Social Security contributes not a single penny to the deficit. Indeed, it is the poster child for fiscal responsibility.”

“Social Security is not in crisis,” declared AARP President Barry Rand in May, urging the deficit commission to avoid addressing the program.

At last month’s Nevada Democratic Convention, Reid got into the act, too. "One of the myths around here is Social Security is in deep trouble,” Reid said, according to the Las Vegas Review-Journal. “Social Security is not in deep trouble. If we did nothing with it, it would be OK for the next 40 years. Now we want to make sure it is OK for the next 40 years."

Those who deny that Social Security is facing a crisis rely on a series of specious arguments. The first is to put the focus on 2037 -- the year the Social Security Trustees project the program’s “trust fund” to be exhausted, rather than 2016, when the program is expected to start running annual deficits. But to draw such a distinction is to pretend that all of the money doesn’t ultimately come from the same bank account (or in this case, the collective bank accounts of American taxpayers).

The Social Security program is financed primarily by payroll taxes. When the amount of tax revenue collected exceeds benefits, the surplus is theoretically put in the trust fund. But in reality, the federal government uses that surplus to finance ongoing government operations, and puts a stack of bonds -- or IOUs -- in the funds instead. So, while it’s true that for about 27 years, there’s theoretically enough money within the system to keep paying beneficiaries, after 2016, that money will have to come from somewhere -- at a time when the nation is already suffocating under a mountain of debt.

The 2009 Social Security Trustees report concluded that because redeeming bonds held within the trust fund will need to come from the general treasury, “Pressures on the Federal Budget will thus emerge well before 2037.”

Further along these lines, the Congressional Budget Office, in a report released earlier this month, wrote that the government bonds held within the trust fund, “are an asset to the Social Security system but a liability to the rest of the government. The resources to redeem government securities in the (Old age, Survivors, and Disability Insurance) trust funds and thereby pay for Social Security benefits in some future year must be generated from taxes, other government income, or government borrowing in that year.”

Specifically, the CBO estimates that by 2020, Social Security will be running a deficit of 0.3 percent of GDP. If you were to apply that percentage to 2009’s GDP -- the most recent year for which actual data is available -- it would represent $42.7 billion. That’s roughly the equivalent of the entire budget of the Department of Homeland Security. And between 2020 and 2040, that deficit is projected to more than quadruple, to 1.3 percent of GDP, or $185 billion if translated into 2009 GDP terms.

Not having a plan to fix the Social Security crisis also makes the bond markets more nervous, which could drive up the government's borrowing costs in the short term.

The other argument made by those who deny a Social Security crisis is that the real crisis is the one facing Medicare and Medicaid due to rising health care costs. It’s undeniable that the health care spending crisis is worse (and that’s been further exacerbated by the passage of the national health care law). But that says more about the severity of the problems facing Medicare and Medicaid than about the solvency of Social Security.

"There can be some tweaks done," Reid himself said. "Stop trying to frighten people about Social Security."

While it is true that Social Security lends itself to a combination of smaller fixes such as raising the retirement age, limiting payouts to wealthier retirees who don’t depend on Social Security for their livelihoods, or pegging the growth in benefits to a lower rate of inflation, anybody who proposes such fixes is typically subjected to the same sort of attacks that Reid has been leveling against Angle. And the longer action is delayed, the more drastic the solution will need to be.

Interestingly, during the campaign, Obama’s proposal for Social Security was to slap those earning more than $250,000 with an additional payroll tax (right now, payroll taxes only affect salary up to $106,800). The problem is, Democrats already dipped into that well when they introduced a similar tax to fund ObamaCare.

Those who seek to preserve the unsustainable status quo in Social Security like to see themselves as defenders of senior citizens. In reality, they’ve declared war against America’s youth. If there's any hope for putting the nation on a sustainable fiscal path, this will have to be proven a failed political strategy.

Can the US economy really return to “business as usual” when it has 4 million houses surplus to requirement, when 1 out of 4 mortgages are in negative equity, and when by our calculation, it is burdened with $4 trillion of excess mortgage debt, equivalent to 30% of GDP?

For many years, total mortgage debt consistently and reliably equalled 0.4 times the value of the US housing stock. Intuitively, this average of 0.4 makes perfect sense as every property usually has a mortgage ranging from 0 to 0.9 times its value. So in 1990, $6 trillion of housing collateral could support $2.5 trillion of mortgages, and by 2006, $23 trillion of housing collateral could support $10 trillion of mortgages. But since then, the US housing stock’s value has slumped to $16 trillion which means the amount of mortgage lending supportable by the collateral has plunged to $6 trillion. However, actual mortgage debt has remained at $10 trillion – $4 trillion too high.

The fact that mortgage debt has barely declined suggests that relatively few homeowners have defaulted on their mortgages or paid off debt yet. Instead, a quarter of all borrowers are sitting on negative equity. That’s just as well – because were mortgage debt to shrink by even half of $4 trillion, the US economy would slump.

Perhaps homeowners are patiently expecting house prices to rise again. But if so, they may be in for a long wait. Prices are likely to be weighed down by a massive oversupply of homes relative to underlying demographic demand. Whether you look at the houses to population ratio, the houses to household ratio or vacant houses ratio, the conclusion is the same – there is a 3% surplus of properties, equivalent to 4 million homes. And with household formation running at just 0.9 million while the US is still building 0.6 million new homes annually, only 0.3 million of the oversupply will be absorbed per year (see page 5).

Ultra low rates to stay

A recent study by the Federal Reserve (The Depth of Negative Equity and Mortgage Default Decisions by Bhutta, Dokko and Shan) investigated the question: at what point do underwater homeowners “strategically default” on their mortgages? Surprisingly, it found that the average borrower doesn’t walk away from his home until negative equity reaches a very high level, -62%. But the fascinating thing was that there was something that could trigger underwater borrowers to default much, much earlier – and that something was an interest rate rise.

With a quarter of US mortgages underwater, and likely to stay that way for some time, the Fed must follow its own research if it wants to prevent a cascade of defaults. Hence, expect US interest rates to stay ultra low for an ultra long time. > >

For many years, total mortgage debt consistently and reliably equalled 0.4 times the value of the US housing stock. Intuitively, this average of 0.4 makes perfect sense as every property usually has a mortgage ranging from 0 to 0.9 times its value. So in 1990, $6 trillion of housing collateral could support $2.5 trillion of mortgages, and by 2006, $23 trillion of housing collateral could support $10 trillion of mortgages. But since then, the US housing stock’s value has slumped to $16 trillion which means the amount of mortgage lending supportable by the collateral has plunged to $6 trillion. However, actual mortgage debt has remained at $10 trillion – $4 trillion too high. >

Loan to value ratio is 1.5 times too high

>

To put it another way, the loan to value ratio of total mortgages outstanding to housing stock value is currently 1.5 times too high. >

24% of US mortgages are underwater

>

The fact that mortgage debt has barely declined suggests that relatively few homeowners have defaulted on their mortgages or paid off debt yet. Instead, a quarter of all borrowers are sitting on negative equity. >

Higher interest rates may trigger cascade of defaults

>

A recent study by the Federal Reserve investigated the central question: at what point do underwater homeowners “strategically default” on their mortgages? Surprisingly, it found that when the decision is based on negative equity alone, the average borrower doesn’t walk away from his home until it is very underwater (negative equity of 62%). But the fascinating thing was that there was something that could trigger underwater borrowers to default much, much earlier – and that something was an interest rate rise. In fact, higher interest rates were even more significant in triggering defaults than higher unemployment.

With a quarter of US mortgages underwater, the Fed must heed the advice of its own research if it wants to prevent a cascade of defaults and the consequent repercussions on the financial system and the economy. Hence, expect US interest rates to stay ultra low until millions of mortgages escape out of negative equity. >

The US has built far too many houses

>

Perhaps homeowners suffering negative equity are patiently expecting house prices to rise again. But they may be in for a long wait. Prices are likely to be weighed down by a massive oversupply of homes relative to underlying demographic demand.

Between 2002 and 2006, US homebuilders went on a construction binge, building 12 million new homes while the number of households went up by just 7 million. The painful legacy is a massive oversupply of houses relative to the number of households. >

The oversupply will take years to clear

>

With household formation running at just 0.9 million while the US is still building 0.6 million new homes annually, only 0.3 million of the oversupply will be absorbed per year. As there are currently 4 million too many homes, it may take years to mop up the huge oversupply of houses.

OregonLive reports PERS rates for state agencies will more than double in 2011.

The actuary for Oregon's Public Employee Retirement System confirmed Friday what is already a common-knowledge piece of the state's looming budget shortfall: the cost of funding PERS will increase sharply in 2011.

Mercer Inc. told the PERS board Friday that systemwide, the payroll rates paid by cities, counties, school districts and state agencies to cover their employees' pension and health care benefits will more than double in 2011, from their current level 5.2 percent of payroll to 10.8 percent of payroll.

As of Dec 31, the retirement system had 76 cents in assets for every $1 in liabilities, excluding prepaid contributions. The system's investments declined about 1 percent year through May 31, Mercer said. If they finish the year at this level, the system's overall funded status, excluding prepaid contributions, will decline to about 70 percent, Mercer said.

Actual pension rates vary by individual employer. Employers will learn the exact rate they'll start paying in 2011 in September. If we finish the year her the system will only be 70% funded. Pray tell what happens if the stock market finished the year down a modest 15% and is flat next year?

Notice the article says "Actual pension rates vary by individual employer". Although the rates will vary, it is not "employers" who pick up the tab. Rather it is taxpayers who have to pay taxes to pick up the tab.

If articles like the one quoted explained things properly, there would be much more needed outrage.

The system is broke and the only way to fix it is to get rid of it. Defined benefit plans at taxpayer expense have to go.

Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com

These kind of situations I have been preaching about for years! All these public plans have the most ridiculous and unattainable assumptions for growth rates and therefore are all amazingly underfunded. When you have an assumed growth rate of 6-8% annually (which almost all of these funds do) your present value of your future liabilities goes way down. When you do not attain those rates of growth you get a dramatically underfunded pension. I have been saying we are probably going to see a range bound market for the next 3-5 years and these funds will become pretty much insolvent.

Fiscal Policy: Many voters are looking forward to 2011, hoping a new Congress will put the country back on the right track. But unless something's done soon, the new year will also come with a raft of tax hikes — including a return of the death tax — that will be real killers.

Through the end of this year, the federal estate tax rate is zero — thanks to the package of broad-based tax cuts that President Bush pushed through to get the economy going earlier in the decade.

But as of midnight Dec. 31, the death tax returns — at a rate of 55% on estates of $1 million or more. The effect this will have on hospital life-support systems is already a matter of conjecture.

Resurrection of the death tax, however, isn't the only tax problem that will be ushered in Jan. 1. Many other cuts from the Bush administration are set to disappear and a new set of taxes will materialize. And it's not just the rich who will pay.

The lowest bracket for the personal income tax, for instance, moves up 50% — to 15% from 10%. The next lowest bracket — 25% — will rise to 28%, and the old 28% bracket will be 31%. At the higher end, the 33% bracket is pushed to 36% and the 35% bracket becomes 39.6%.

But the damage doesn't stop there.

The marriage penalty also makes a comeback, and the capital gains tax will jump 33% — to 20% from 15%. The tax on dividends will go all the way from 15% to 39.6% — a 164% increase.

Both the cap-gains and dividend taxes will go up further in 2013 as the health care reform adds a 3.8% Medicare levy for individuals making more than $200,000 a year and joint filers making more than $250,000. Other tax hikes include: halving the child tax credit to $500 from $1,000 and fixing the standard deduction for couples at the same level as it is for single filers.

Letting the Bush cuts expire will cost taxpayers $115 billion next year alone, according to the Congressional Budget Office, and $2.6 trillion through 2020.

But even more tax headaches lie ahead. This "second wave" of hikes, as Americans for Tax Reform puts it, are designed to pay for ObamaCare and include:

The Medicine Cabinet Tax. Americans, says ATR, "will no longer be able to use health savings account, flexible spending account, or health reimbursement pretax dollars to purchase nonprescription, over-the-counter medicines (except insulin)."

This is a blogger that I look forward to every week for his post. He is hilarious and informative. Check out his older posts they are all Gems.

Lately, I have been hinting to my boss that I need a raise to do my job, and she has been hinting that she needs an employee to competently do my job, so you can see how we are temporarily at an impasse in negotiations.

Not so in China, however! The Economist magazine notes that in China, “Wages have been rising at 10-15% annually, but recently workers have begun to demand even heftier increases.”

Well, I am already astonished at this increase in incomes, and to impress you with my facility with the Rule of 72, I calculate with simple division that a 10% increase in wages will double wages in 7.2 years, which you gotta agree is a lot of extra spending power, unless inflation in prices eats it all away, which, unfortunately, it probably will.

And this is compounded by the Chinese economy itself growing by at least 10% a year, too, meaning that the Chinese economy will double in size in that selfsame 7.2 years! Wow!

An economy that is twice as big, and wages that doubled? My Inner Mogambo Economist (IME) immediately sees that this means a lot more consumption!

And turning that interesting fact to our advantage, so that we can hopefully make a lot of money without working, let me ask an instructive question; “Do you honestly think that commodities will go down in price when there is such growing demand, even when you can see by the look on my face and the tone of my voice that I am going to laugh at you and heap Rude Mogambo Scorn (RMS) on your stupid head if you say yes?”

And the boom may be bigger and sooner than that, as we read on Bloomberg.com that “At least nine Chinese provinces and cities raised minimum wages by as much as a third after Premier Wen Jiabao called for measures to head off growing worker unrest in the world’s third-largest economy.”

And it gets more delicious when Gary Gibson from Whiskey & Gunpowder interviewed Chris Mayer, who said that in “the next five years or so,” that China will gain “almost 400 million middle class consumers.”

The Really, Really Important Thing (RRIT) about this particular statistic is that 400 million new middle class Chinese people is more people than the entire population of the United States!

Perhaps now you are beginning to understand why the 21st century is going to be about the Chinese and what the Chinese want to consume in prodigious amounts, especially when the yuan starts gaining strength to make imports cheaper.

To put it in perspective, Mr. Mayer says, “when you think about China, they’re the largest incremental buyer of just about any commodity you’d care to name, so a stronger renminbi means that they have more purchasing power to buy iron ore and coal and oil and all the other things they need. That could be an extra little fire under commodity prices.”

Commodities? China? It is here that I began to think of Chinese food, and the next thing I knew, I went out to get some, hoping to get a seat before 400 new middle-class Chinese consumers started getting in line ahead of me at the restaurant.

As soon as I thought about it, of course, I realized that this won’t happen, says Chris, for 5 years, so since I had an extra few minutes, I whirled the Mogambo-Mobile around (“screech!”) and stopped (“screech!”) to buy more gold, silver and oil as both a guaranteed reaction from my wife (“screech!”) and as a guaranteed play on commodities, as gold, silver and oil are a Big Bold Bet (BBB) against the government and the Federal Reserve succeeding at creating, borrowing and spending more money to “fix” the massive, bankrupting problems caused by creating, borrowing and spending too much money, a hopeless task so daunting that no other dirtbag government has ever succeeded, at least none in the last 4,500 years of dirtbag governments borrowing and spending themselves into bankruptcy while twisting their economies into huge, distorted, malignant, parasitical nightmares of government domination and funding.

In other words, “Whee! This investing stuff is easy!”

And, I am happy to report, it goes well with Chinese food, too!

Has there been significant deleveraging in the US housing market? Not really. Instead, with already $7 trillion in home equity lost, mortgages have come down only $270 billion. It’s a significant discrepancy that’s going to have to come into alignment somehow.

Jesse’s Café Américain explains:

“This debt must be resolved. There are two major ways to do it: repayment and default.

“Repayment is probably a fantasy, if not beating a dead horse. The homeowners do not have the money with which to pay the loans given the current state of employment and wage stagnation, and the mortgages are for the most part on houses whose value is significantly under water compared to the debt, as in ‘ just mail in the keys.’

“Straight up default, writing off the debt even through foreclosure, is also probably out of the question, because it would essentially vaporize the balance sheet of the US banking system which is also insolvent, to a greater degree than most understand, and if they understand it, would admit.”

This is while of “986 bank holding companies in the US, 980 [banks] lost money last year. The lucky six were the TBTF banks on major government subsidy.” To support his thinking, Jesse goes on to cite an Automatic Earth piece, Is It Time to Storm the Bastille Again:

“That is, what Americans’ homes are worth, their equity, decreased by $7 trillion — from $20 trillion to $13 trillion, from spring 2006 to spring 2010. In the same period, mortgage debt, what Americans owe on their homes, went down by only $270 billion. Yes, that’s right: US homeowners lost more, by a factor of 26, than they ‘gained’ through clearing mortgage debt. Thus, if we estimate that there are 75 million homeowners in America, they all, each and every one of them, lost $93,333.”

The government bailouts, already a failed experiment, didn’t help the vast majority of banks get profitable and also aren’t going to help homeowners pay mortgages. This debt isn’t looking to be liquidated without a prolonged period of tough times. You can read more details in Jesse’s Café Américain’s coverage of unresolved debt in the US financial system.

Thought this was particularly interesting. From David Rosenberg:

"Everyone complains about government manipulation of the data -- how "hedonics" skew the numbers (like GDP and CPI). But what about the stock market? I'm not saying it's "manipulated" but it does have substantial "survivorship bias" -- especially after a gut wrenching recession. Just cleaning the failures out of the system and erasing them from the S&P 500, from WaMu, to Wachovia, to Bear Stearns, to Lehman, to Fannie and Freddie, and replacing them with companies that survived, was responsible for nearly 40% of the rally in the market off the 2009 lows. Think about that, if those firms who went under were still in the index, according to some help from a strategy friend at an aforementioned bank, the S&P 500 would be trading closer to 900 today than 1,100."

Notable quotes for those who don't want to watch the video

Grant's thoughts on new Fed additions:

"I think the first order of business will be to try once more to print enough dollars to make something happen in the U.S. economy.”

On San Francisco Fed President Janet Yellen:

“Janet Yellen has had 36 opportunities to vote on monetary policy at the Federal Open Market Committee and she has voted ‘Aye, yes’ 36 times. 36 for 36 times. Now, has the Fed been right 36 consecutive times? No. I think that Janet Yellen is a well credentialed, consensus-hugging economist straight out of the Fed HR department. She is ideal from the point of view of the Fed bureaucracy. She will make not one ripple.”

On MIT economist Steve Diamond and Maryland state banking regulator Sarah Bloom Raskin:

“I’ve never met them but I suppose they are charming. They certainly are well credentialed. They may well have an avocation in monetary theory, but that is not their vocation. Their vocation, in the case of Professor Diamond, is fiscal policy, pensions, social security, he is an authority. He's mentor of Ben Bernanke so he’s a formidable academic.”

"Sarah Bloom Raskin is a formidable regulator. But neither is a formidable thinker about the nature of money or about the history of money or about how the Fed might paradoxically make things worse by doing what it does trying to make things better, which I think is the great question. These are people who, I think, are unlikely to oppose novel solutions to our fundamental monetary dilemma which is that the U.S. dollar is a faith-based currency of no intrinsic value that is manipulated by the Fed and the consequences of the manipulation are often quite different from what was intended. That’s the problem.”

On Fed monetary policy:

"Deflation is a funny thing. It's a word that is much in the news, much in the markets, but is all too infrequently to find. So the Fed says that deflation is broadly declining prices. But could not also be progress? In other words, if the world produces more at lower prices, is that so bad? Americans spend half of their weekends, it seems, looking for bargains.”

"So the Fed is telling us that bargains galore is something that the Fed must resist with radical volumes of credit creation… I guess what I would ask the Fed is would it please stop and help us understand why this is bad? So in 2002 and 2003, Alan Greenspan, then chairman, and Ben Bernanke, then a newly fledged governor, were out giving speeches saying that deflation is a clear and present danger, and we must - they said at the Fed - must cut rates dramatically, which they did to 1 percent."

"But the price indices today are much weaker than they were in 2003. So where is the Fed? Why not broach the topic of deflation again?"

"So what I blame the Fed for, among other things, is a lack of intellectual rigor and forthrightness."

On Federal Reserve Chairman Ben Bernanke:

"I think this is not being forthcoming with us, the people, about the nature of his concerns."

"In 2003, he was all deflation all the time. Well now the Cleveland Fed's median CPI was like 1.7 percent year-over-year, now it's 0.5 percent year-over-year. So where is the concern?"

"I think the concern will surface. We'll see more on Friday when the CPI comes out. But I think something ahead of the markets is a likelihood of the Fed stepping on the gas once more, so called quantitative easing - I think that's likely to happen…The Fed is already clearing its throat. You can see this in the newspaper leaks."

For all of its wild popularity, caffeine is one seriously misunderstood substance. It's not a simple upper, and it works differently on different people with different tolerances—even in different menstrual cycles. But you can make it work better for you. Photo by rbrwr.

We've covered all kinds of caffeine "hacks" here at Lifehacker, from taking "caffeine naps" to getting "optimally wired." And, of course, we're obsessed with the perfect cup of coffee. But when it comes to why so many of us love our coffee, tea, soda, or energy drink fixes, and what they actually do to our busy brains, we've never really dug in. While there's a whole lot one can read on caffeine, most of it falls in the realm of highly specific medical research, or often conflicting anecdotal evidence. Luckily, one intrepid reader and writer has actually done that reading, and weighed that evidence, and put together a highly readable treatise on the subject. Buzz: The Science and Lore of Alcohol and Caffeine, by Stephen R. Braun, is well worth the short 224-page read. It was released in 1997, but remains the most accessible treatise on what is and isn't understood about what caffeine and alcohol do to the brain. It's not a social history of coffee, or a lecture on the evils of mass-market soda—it's condensed but clean science.

What follows is a brief explainer on how caffeine affects productivity, drawn from Buzz and other sources noted at bottom. We also sent Braun a few of the questions that arose while reading, and he graciously agreed to answer them.

Caffeine Doesn't Actually Get You Wired

Right off the bat, it's worth stating again: the human brain, and caffeine, are nowhere near totally understood and easily explained by modern science. That said, there is a consensus on how a compound found all over nature, caffeine, affects the mind. Every moment that you're awake, the neurons in your brain are firing away. As those neurons fire, they produce adenosine as a byproduct, but adenosine is far from excrement. Your nervous system is actively monitoring adenosine levels through receptors. Normally, when adenosine levels reached a certain point in your brain and spinal cord, your body will start nudging you toward sleep, or at least taking it easy. There are actually a few different adenosine receptors throughout the body, but the one caffeine seems to interact with most directly is the A1 receptor. More on that later. Enter caffeine. It occurs in all kinds of plants, and chemical relatives of caffeine are found in your own body. But taken in substantial amounts—the semi-standard 100mg that comes from a strong eight-ounce coffee, for instance—it functions as a supremely talented adenosine impersonator. It heads right for the adenosine receptors in your system and, because of its similarities to adenosine, it's accepted by your body as the real thing and gets into the receptors. Update: Commenter dangermou5e reminds us of web comic The Oatmeal's take on adenosine and caffeine. It's concise: More important than just fitting in, though, caffeine actually binds to those receptors in efficient fashion, but doesn't activate them—they're plugged up by caffeine's unique shape and chemical makeup. With those receptors blocked, the brain's own stimulants, dopamine and glutamate, can do their work more freely—"Like taking the chaperones out of a high school dance," Braun writes in an email. In the book, he ultimately likens caffeine's powers to "putting a block of wood under one of the brain's primary brake pedals."

It's an apt metaphor, because it spells out that caffeine very clearly doesn't press the "gas" on your brain, and that it only blocks a "primary" brake. There are other compounds and receptors that have an effect on what your energy levels feel like—GABA, for example—but caffeine is a crude way of preventing your brain from bringing things to a halt. "You can," Braun writes, "get wired only to the extent that your natural excitatory neurotransmitters support it." In other words, you can't use caffeine to completely wipe out an entire week's worth of very late nights of studying, but you can use it to make yourself feel less bogged down by sleepy feelings in the morning.

These effects will vary, in length and strength of effect, from person to person, depending on genetics, other physiology factors, and tolerance. But more on that in a bit. What's important to take away is that caffeine is not as simple in effect as a direct stimulant, such as amphetamines or cocaine; its effect on your alertness is far more subtle.

It Boosts Your Speed, But Not Your Skill—Depending on Your Skill Set

Johann Sebastian Bach loved him some coffee. So did Voltaire, Balzac, and many other great minds. But the type of work they did didn't necessarily get a boost from their prodigious coffee consumption—unless their work was so second-nature to them that it felt like data entry.

The general consensus on caffeine studies shows that it can enhance work output, but mainly in certain types of work. For tired people who are doing work that's relatively straightforward, that doesn't require lots of subtle or abstract thinking, coffee has been shown to help increase output and quality. Caffeine has also been seen to improve memory creation and retention when it comes to "declarative memory," the kind students use to remember lists or answers to exam questions.

(In a semi-crazy side note we couldn't resist, researchers have implied this memory boost may be tied to caffeine's effect on adrenaline production. You have, presumably, sharper memories of terrifying or exhilarating moments in life, due in part to your body's fight-or-flight juice. Everyone has their "Where I was when I heard that X died" story, plugging in John F. Kennedy, John Lennon, or Kurt Cobain, depending on generational relatability).

Then again, one study in which subjects proofread text showed that a measurable boost was mainly seen by those who could be considered "impulsive," or willing to sacrifice accuracy and quality for speed. And the effect was only seen in morning tests, indicating the subjects may have either become lightly dependent on caffeine, or were more disposed to such tasks at that time of day.

So when it comes to caffeine's effects on your work, think speed, not power. Or consider it an unresolved question. If we're only part of the way to understanding how caffeine affects the brain, we're a long way to knowing exactly what kind of chemicals or processes are affected when, say, one writes a post about caffeine science one highly caffeinated afternoon.

For a more direct look at what happens to your brain when there's caffeine in your system, we turn to the the crew at Current. They hooked up one of their reporters to a brain monitor while taking on some new caffeine habits, and share their brains on caffeine:

Effectiveness, Tolerance, and Headaches

Why do so many patients coming out of anesthesia after major surgery feel a headache? It's because, in most cases, they're not used to going so long without coffee. The good news? If they wait a few more days, they can start saving coffee again for when they really need it.

The effectiveness of caffeine varies significantly from person to person, due to genetics and other factors in play. The average half-life of caffeine—that is, how long it takes for half of an ingested dose to wear off—is about five to six hours in a human body. Women taking oral birth control require about twice as long to process caffeine. Women between the ovulation and beginning of menstruation see a similar, if less severe, extended half-life. For regular smokers, caffeine takes half as long to process—which, in some ways, explains why smokers often drink more coffee and feel more agitated and anxious, because they're unaware of how their bodies work without cigarettes. As one starts to regularly take in caffeine, the body and mind build up a tolerance to it, so getting the same kind of boost as one's first-ever sip takes more caffeine—this, researcher can agree on. Exactly how that tolerance develops is not so clear. Many studies have suggested that, just as with any drug addiction, the brain strives to return to its normal function while under "attack" from caffeine by up-regulating, or creating more adenosine receptors. But regular caffeine use has also been shown to decrease receptors for norepinephrine, a hormone akin to adrenaline, along with serotonin, a mood enhancer. At the same time, your body can see a 65 percent increase in receptors for GABA, a compound that does many things, including regulate muscle tone and neuron firing. Some studies have also seen changes in different adenosine receptors when caffeine becomes a regular thing.

Caffeine, it's been suggested, is probably not directly responsible for all these changes. By keeping your brain from using its normal "I'm tired" sensors, though, your caffeine may be causing the brain to change the way all of its generally excitable things are regulated. Your next venti double shot goes a little less far each time, in any case. Photo by zoghal.

A 1995 study suggests that humans become tolerant to their daily dose of caffeine—whether a single soda or a serious espresso habit—somewhere between a week and 12 days. And that tolerance is pretty strong. One test of regular caffeine pill use had some participants getting an astronomical 900 milligrams per day, others placebos—found that the two groups were nearly identical in mood, energy, and alertness after 18 days. The folks taking the equivalent of nine stiff coffee pours every day weren't really feeling it anymore. They would feel it, though, when they stopped.

You start to feel caffeine withdrawal very quickly, anywhere from 12 to 24 hours after your last use. That's a big part of why that first cup or can in the morning is so important—it's staving off the early effects of withdrawal. The reasons for the withdrawal are the same as with any substance dependency: your brain was used to operating one way with caffeine, and now it's suddenly working under completely different circumstances, but all those receptor changes are still in place. Headaches are the nearly universal effect of cutting off caffeine, but depression, fatigue, lethargy, irritability, nausea, and vomiting can be part of your cut-off, too, along with more specific issues, like eye muscle spasms. Generally, though, you'll be over it in around 10 days—again, depending on your own physiology and other factors. Update: Commenter microinjectionist offers his own summary of more recent caffeine studies, which offers expanded reasons why caffeine users feel a "morning crash," as well as why your whole body, not just your brain, might feel so bad when you withdraw.

Getting Out of the Habit and Learning to Tame Caffeine

Beyond the equivalent of four cups of coffee in your system at once, caffeine isn't giving you much more boost—in fact, at around the ten-cup level, you're probably less alert than non-drinkers. So what if you want to start getting a real boost from caffeine once again, in a newly-learned, less-dependent way? Our own Jason Fitzpatrick has both intentionally "quit" caffeine, as well as just plain run out of coffee. Being the kind of guy who measures his own headaches and discomfort, he suggests measuring your caffeine intake, using caffeine amounts in all your drinks, chocolate, and other "boosting" foods. Wise Bread has a good roundup of caffeine amounts, and the Buzz Vs. The Bulge chart also shows how many calories you'll be cutting if you start scaling back. Once you know your levels, map out a multi-week process of scaling down, and stick to it. Jason also suggests that dependency kicking is a good time to start taking walks, doing breathing exercises, or other mind-clearing things, because, in his experience, their effects are much greater when caffeine is not so much a part of your make-up.

Braun, author of Buzz, sees it the same way, but still uses coffee—strategically, according to our email exchange:

In practical terms, this means that if you'd like to be able to turn to caffeine when you need it for a quick, effective jolt, it's best to let your brain "dry out" for at least several days prior to administration. This is actually my current mode of consumption. I don't regularly drink coffee anymore (gasp).

This from a man who loved (and wore out) his home espresso maker. I love coffee in all its guises. But after 30+ years it wasn't working for me. For one thing, the problem with caffeine is that there are adenosine receptors all over the body, including muscles. For me, that meant that caffeine made me vaguely stiff and sore, and it aggravated a tender lower back that was prone to spasm. But I also just wasn't getting a clean, clear buzz from coffee...I drank so much, so regularly, that drinking an extra cup or two didn't do a helluva lot except, perhaps, make me a little more irritable.

So about a year ago I slowly tapered down, and now I have, if anything, a cup of tea (half black, half peppermint) in the morning. (The amount of caffeine from the black tea isn't enough to wire a gnat.) Not only does my body feel better now, my brain is clean of caffeine, so I really want (or need) a good neural jump-start, I will freely...nay, ecstatically...indulge. Then I stop and let the brain settle again.

That's the theory, anyway...and it's basically true, although I'll freely admit that sometimes I have an espresso or coffee just because it tastes so damned good.

If you'd like Braun's extended takes on caffeine tolerance and withdrawal, along with the advent of energy drinks and caffeine's impact on creativity, you can read our full email interview.

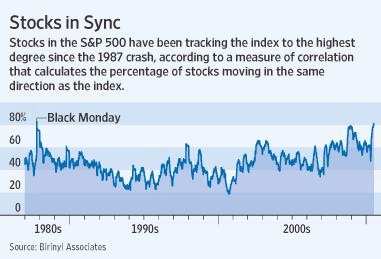

The Wall Street Journal notes that stocks are trading in lock-step more than at any time since the 1987 crash. Please consider The Herd Instinct Takes Over. Which has some very interesting data but the conclusion is a little off......

In recent weeks, stocks in the Standard & Poor's 500-stock index have shown an increasing tendency to move in the same direction at the same time. Last week, those stocks' tendency to move in the same direction as the index hit an extreme not seen since October 1987, according to research by investment group Birinyi Associates in Westport, Conn.

The average correlation since 1980 has been 44%. But by mid-June, the correlation had jumped back above 70%, as investors stopped looking for winners and just sold broadly. Last week it surpassed its 2008 high of 79% and hit 81%, the highest level since the 1987 crash, when it touched 83% for one day. That means that on most days recently, the great majority of stocks in the S&P 500 were moving in the same direction, up or down.

Correlation typically goes up during volatile periods, reflecting investors' tendency to dump stocks wholesale rather than try to pick out stocks that once were viewed as refuges, such as those that pay dividends.

Volume has been anemic during this rise, with little individual participation. So did "herding" take over or did black-box futures and flash-trading take over? I'm thinking its the latter

This article, combined with Grantham's 1Q commentary on the Graham and Dodd Style investing has really confirmed my feelings on how this stock market has been acting and how it will continue to act in the future. Too much meddling by the government has ruined tried and true value investing.

When I read Security Analysis, the investment bible by Graham and Dodd, I am transported to a past era when investment life was easier. You could focus your energies on finding companies trading at less than fair value. You focused on the balance sheet and the income statement. The economy was static. It grew a few percent a year and economic life was rather uneventful. There were panics and crashes, but these were usually confined to certain industries like railroads where there had been overexpansion. Most companies were immune to these economic disturbances.

Graham and Dodd could look at the Dollars on the balance sheet and feel confident that they would not be marginalized by the next round of quantitative easing. They didn’t have to worry about the fiscal sanity of their government. It was just taken for granted that the US government finances were solvent. Governments always enacted arbitrary laws, but no one had to worry about wholesale regulatory change every time congress was in session. Regulatory regimes changed gradually—if at all. Liabilities were what showed up on your balance sheet. An investor did not have to worry about wolf-packs of ambitious lawyers descending on every company in crisis and exacting an extra pound of flesh. Tax rates were constant enough to allow for long term economic planning.

Prudent investors demanded a margin of safety before investing in a company. That margin of safety protected you from all of the above and still left plenty of room for upside. That is because most of the risks to a corporation were quantifiable. This let investors focus on their companies and ignore the newspapers. The macro world was largely irrelevant. You bought great companies at reasonable prices and waited until the share prices appreciated. World events simply didn’t matter. The business cycle only barely mattered. Buy cheap and let compounding work in your favor.

Now, investing seems to revolve around just one factor. What will the government do next? Which businesses will they clamp down on? Which will be subsidized? Who will get the next bailout? Will various tax subsidies be increased or eliminated? What new laws are in the mix? How can you anticipate all these changes?

There are no constants any longer. You cannot rely on anything. Everything seems perpetually in flux. The world economy is once again imploding. Will it be allowed to collapse? Unlikely. When will the next bailout be announced? What shape will it take? Who will the winners be? That really is the question that everyone demands an answer to. When is the next bailout? Bigger, Badder, More Corrupt—that’s our country’s new mantra. Which companies will lobby the right congressmen and be included? Which will be destroyed?

How do you invest in an environment like this? Say you look at a company. Do you want a business that’s economically sensitive—or one that has a strong and liquid balance sheet? Are you betting on them printing just a little money—or a full out Weimar style debasement? What’s the expected tax rate? It’s going up. That’s for sure. Will carbon taxes impact my businesses? What about changes in health care legislation? There are dozens of issues currently debated in congress. They all impact businesses.

Then there’s the whole wide world outside of the US. A generation ago, most businesses were regional. You could ignore what happened in China. Now China is the lynchpin of global economic growth. How can you decipher China? It’s monolithic. Will the Euro survive? Will it be debased or discarded as the component nations go their own separate way? Imagine the world’s largest economic bloc simply repudiating their currency? How do you invest for that? The whole investment climate is a daisy-chain of binary outcomes that are mutually exclusive. The middle ground seems vanquished.

These are the issues that I tango with daily. I invest in small businesses. Over the past decade, I’ve made a lot of money doing this. However, it continues to become more difficult. The rules change every day. A decade ago, I mostly ignored the macro—now I spend most of my time analyzing it. Small companies are illiquid and volatile. That has never bothered me before. Now I increasingly want more liquidity. I want the ability to react to the newest crisis. I am not a trader—now I have no choice. Every morning, I have to throw out all the old rules and start again. The macro events rule—businessmen are impotent.

I want to buy great businesses and put them away for years at a time. No longer can you trust that a dominant business will remain dominant. It won’t be a competitor that destroys the business. It will be an errant politician or a bad hedge on their Euro exposure. Volatility is destroying real businesses. Is every company now expected to hire whole trading desks to manage various exposures? How can you expect the most basic elements of a business to remain stable when the currency itself is increasingly detached from reality?

I have no problem navigating economic booms and collapses. That’s part of investing. What I strongly object to is the government increasingly inserting itself into the economy. You cannot manage an economy based on the applause meter of 24-hour news programs. You cannot manage an economy. Period. It is not debatable. Unfortunately, our government continues to corral the various market forces and lead them towards whatever myopic utopia politicians think will be needed for reelection. This creates economic anarchy. If you could run an economy based on erratic rules and crony capitalism, Argentina would be a world power. If you could print your way to prosperity, Zimbabwe would be a world banking hub. If you could command the economy to heed you, the USSR would still exist. I’m scared that world leaders have taken all the worst lessons of the last generation of economic thought and bundled them together into some sort of economic doomsday machine.

I apologize for this stream of consciousness. I’m frustrated. For my whole career, I believed that a great business with a strong return on capital would outperform all other asset classes. What if that isn’t true? For the past three years, only the macro has mattered. Going forward, what if the macro is ALL that matters? What if you have to rapidly jump from asset class to asset class as the rules change weekly? I hope this isn’t the case. However, it is time to consider that possibility.

In an age of increasing uncertainty, market multiples will collapse. Investors will demand an even larger margin of safety. Earnings will become increasingly volatile. Investors will focus more and more on the balance sheet. Unfortunately, most companies trade at many times book value. Some of the largest companies in the US have negative tangible book value. I expect to see market multiples continue to decline. Why would you risk your capital in uncertain times when you can just buy gold and ignore all the chaos around us? That’s really what I wrestle with the most. Gold will continue to go higher over time—if only because world governments seem determined to act foolish. Can you find companies that will outpace the price increase of gold? It will be difficult. The macro forces arrayed against business are just that extreme. You can no longer ignore the macro. The macro outweighs all else now.

For all of its wild popularity, caffeine is one seriously misunderstood substance. It's not a simple upper, and it works differently on different people with different tolerances—even in different menstrual cycles. But you can make it work better for you.

For all of its wild popularity, caffeine is one seriously misunderstood substance. It's not a simple upper, and it works differently on different people with different tolerances—even in different menstrual cycles. But you can make it work better for you. While there's a whole lot one can read on caffeine, most of it falls in the realm of highly specific medical research, or often conflicting anecdotal evidence. Luckily, one intrepid reader and writer has actually done that reading, and weighed that evidence, and put together a highly readable treatise on the subject.

While there's a whole lot one can read on caffeine, most of it falls in the realm of highly specific medical research, or often conflicting anecdotal evidence. Luckily, one intrepid reader and writer has actually done that reading, and weighed that evidence, and put together a highly readable treatise on the subject.  Every moment that you're awake, the neurons in your brain are firing away. As those neurons fire, they produce

Every moment that you're awake, the neurons in your brain are firing away. As those neurons fire, they produce  Enter

Enter

More important than just fitting in, though, caffeine actually binds to those receptors in efficient fashion, but doesn't activate them—they're plugged up by caffeine's unique shape and chemical makeup. With those receptors blocked, the brain's own stimulants,

More important than just fitting in, though, caffeine actually binds to those receptors in efficient fashion, but doesn't activate them—they're plugged up by caffeine's unique shape and chemical makeup. With those receptors blocked, the brain's own stimulants,  Johann Sebastian Bach loved him some coffee. So did Voltaire, Balzac, and many other great minds. But the type of work they did didn't necessarily get a boost from their prodigious coffee consumption—unless their work was so second-nature to them that it felt like data entry.

Johann Sebastian Bach loved him some coffee. So did Voltaire, Balzac, and many other great minds. But the type of work they did didn't necessarily get a boost from their prodigious coffee consumption—unless their work was so second-nature to them that it felt like data entry. As one starts to regularly take in caffeine, the body and mind build up a tolerance to it, so getting the same kind of boost as one's first-ever sip takes more caffeine—this, researcher can agree on. Exactly how that tolerance develops is not so clear. Many studies have suggested that, just as with any drug addiction, the brain strives to return to its normal function while under "attack" from caffeine by up-regulating, or creating more adenosine receptors. But regular caffeine use has also been shown to decrease receptors for

As one starts to regularly take in caffeine, the body and mind build up a tolerance to it, so getting the same kind of boost as one's first-ever sip takes more caffeine—this, researcher can agree on. Exactly how that tolerance develops is not so clear. Many studies have suggested that, just as with any drug addiction, the brain strives to return to its normal function while under "attack" from caffeine by up-regulating, or creating more adenosine receptors. But regular caffeine use has also been shown to decrease receptors for  Our own Jason Fitzpatrick has both intentionally "quit" caffeine, as well as just plain run out of coffee. Being the kind of guy who measures his own headaches and discomfort, he suggests measuring your caffeine intake, using caffeine amounts in all your drinks, chocolate, and other "boosting" foods.

Our own Jason Fitzpatrick has both intentionally "quit" caffeine, as well as just plain run out of coffee. Being the kind of guy who measures his own headaches and discomfort, he suggests measuring your caffeine intake, using caffeine amounts in all your drinks, chocolate, and other "boosting" foods.