| The Daily Show With Jon Stewart | Mon - Thurs 11p / 10c | |||

| The Big Bank Theory | ||||

| ||||

Wednesday, December 8, 2010

John Stewart Catches Ben Bernanke Lying on TV

Classic!!

Saturday, November 13, 2010

Socialsm Taught to High Schoolers

Picture a bunch of high school students taking an algebra test. The high score is 100, the low score was a 75, and the class average is an 88. You let the students vote on the scoring - either everyone receives the grade they earned, or everyone gets the same grade, whatever the average was. the kicker is that you get to vote only once this year, so the decision remains intact for the entire school year.

It's a no brainer for the half that scored below average, and they pick to give everyone the average. Those who got the average or slightly better vote the same way, since it gives them somewhat of a cushion in case they botch one test. For those who scored closer to 100, a few of them are moonbats who figure they can help out those in need. As a result of the voting, everyone gets an 88. I am one who got a 96 and voted against it, but no one cares.

Next week there's another algebra test but the grades slipped a bit, with 96 as the high score, 60 as the low score, and 80 as an average. I am upset by this time, but my opponents point out that people would have failed if it wasn't for us.

In the third week there is another test, and now the high score is 80, the low score is 40, and the average is 60. People start getting upset. By the fourth week, the entire class gets a failing grade and is ready to revolt against the teacher.

Assuming that everyone learned their lesson on the value of socialism, the teacher relents and repeals the decision and announces they'll go back to standard scoring. When some people still fail after this point, even though everyone now gets teh score they earned, they are looking for someone to blame, since it can't possibly their fault.

It's a no brainer for the half that scored below average, and they pick to give everyone the average. Those who got the average or slightly better vote the same way, since it gives them somewhat of a cushion in case they botch one test. For those who scored closer to 100, a few of them are moonbats who figure they can help out those in need. As a result of the voting, everyone gets an 88. I am one who got a 96 and voted against it, but no one cares.

Next week there's another algebra test but the grades slipped a bit, with 96 as the high score, 60 as the low score, and 80 as an average. I am upset by this time, but my opponents point out that people would have failed if it wasn't for us.

In the third week there is another test, and now the high score is 80, the low score is 40, and the average is 60. People start getting upset. By the fourth week, the entire class gets a failing grade and is ready to revolt against the teacher.

Assuming that everyone learned their lesson on the value of socialism, the teacher relents and repeals the decision and announces they'll go back to standard scoring. When some people still fail after this point, even though everyone now gets teh score they earned, they are looking for someone to blame, since it can't possibly their fault.

5 Statements for Today's Economic Times

1. You cannot legislate the poor into prosperity, by legislating the

wealth out of prosperity.

2. What one person receives without working for, another person must

work for without receiving.

3. The government cannot give to anybody anything that the government does not first take from somebody else.

4. You cannot multiply wealth by dividing it.

5. When half of the people get the idea that they do not have to work

because the other half is going to take care of them, and when the other half gets the idea that it does no good to work, because somebody else is going to get what they work for, that is the beginning of the end of the nation.

wealth out of prosperity.

2. What one person receives without working for, another person must

work for without receiving.

3. The government cannot give to anybody anything that the government does not first take from somebody else.

4. You cannot multiply wealth by dividing it.

5. When half of the people get the idea that they do not have to work

because the other half is going to take care of them, and when the other half gets the idea that it does no good to work, because somebody else is going to get what they work for, that is the beginning of the end of the nation.

Wednesday, November 10, 2010

An Incredible Story/Speech

http://www.juntosociety.com/

One day in the House of Representatives a bill was taken up appropriating money for the benefit of a widow of a distinguished naval officer. Several beautiful speeches had been made in its support. The Speaker was just about to put the question when Crockett arose:

"Mr. Speaker--I have as much respect for the memory of the deceased, and as much sympathy for the sufferings of the living, if suffering there be, as any man in this House, but we must not permit our respect for the dead or our sympathy for a part of the living to lead us into an act of injustice to the balance of the living. I will not go into an argument to prove that Congress has not the power to appropriate this money as an act of charity. Every member upon this floor knows it. We have the right, as individuals, to give away as much of our own money as we please in charity; but as members of Congress we have no right so to appropriate a dollar of the public money. Some eloquent appeals have been made to us upon the ground that it is a debt due the deceased. Mr. Speaker, the deceased lived long after the close of the war; he was in office to the day of his death, and I have never heard that the government was in arrears to him.

"Every man in this House knows it is not a debt. We cannot, without the grossest corruption, appropriate this money as the payment of a debt. We have not the semblance of authority to appropriate it as charity. Mr. Speaker, I have said we have the right to give as much money of our own as we please. I am the poorest man on this floor. I cannot vote for this bill, but I will give one week's pay to the object, and if every member of Congress will do the same, it will amount to more than the bill asks."

He took his seat. Nobody replied. The bill was put upon its passage, and, instead of passing unanimously, as was generally supposed, and as, no doubt, it would, but for that speech, it received but few votes, and, of course, was lost.

Later, when asked by a friend why he had opposed the appropriation, Crockett gave this explanation:

"Several years ago I was one evening standing on the steps of the Capitol with some other members of Congress, when our attention was attracted by a great light over in Georgetown. It was evidently a large fire. We jumped into a hack and drove over as fast as we could. In spite of all that could be done, many houses were burned and many families made houseless, and, besides, some of them had lost all but the clothes they had on. The weather was very cold, and when I saw so many women and children suffering, I felt that something ought to be done for them. The next morning a bill was introduced appropriating $20,000 for their relief. We put aside all other business and rushed it through as soon as it could be done.

"The next summer, when it began to be time to think about election, I concluded I would take a scout around among the boys of my district. I had no opposition there, but, as the election was some time off, I did not know what might turn up. When riding one day in a part of my district in which I was more of a stranger than any other, I saw a man in a field plowing and coming toward the road. I gauged my gait so that we should meet as he came to the fence. As he came up, I spoke to the man. He replied politely, but, as I thought, rather coldly.

"I began: 'Well, friend, I am one of those unfortunate beings called

candidates, and---‘

"Yes I know you; you are Colonel Crockett. I have seen you once before, and voted for you the last time you were elected. I suppose you are out electioneering now, but you had better not waste your time or mine, I shall not vote for you again."

"This was a sockdolager...I begged him to tell me what was the matter.

" ‘Well, my friend; I may as well own up. You have got me there. But certainly nobody will complain that a great and rich country like ours should give the insignificant sum of $20,000 to relieve its suffering women and children, particularly with a full and overflowing Treasury, and I am sure, if you had been there, you would have done just as I did.'

" ‘It is not the amount, Colonel, that I complain of; it is the principle. In the first place, the government ought to have in the Treasury no more than enough for its legitimate purposes. But that has nothing with the question. The power of collecting and disbursing money at pleasure is the most dangerous power that can be entrusted to man, particularly under our system of collecting revenue by a tariff, which reaches every man in the country, no matter how poor he may be, and the poorer he is the more he pays in proportion to his means. What is worse, it presses upon him without his knowledge where the weight centers, for there is not a man in the United States who can ever guess how much he pays to the government. So you see, that while you are contributing to relieve one, you are drawing it from thousands who are even worse off than he. If you had the right to give anything, the amount was simply a matter of discretion with you, and you had as much right to give $20,000,000 as $20,000. If you have the right to give to one, you have the right to give to all; and, as the Constitution neither defines charity nor stipulates the amount, you are at liberty to give to any and everything which you may believe, or profess to believe, is a charity, and to any amount you may think proper. You will very easily perceive what a wide door this would open for fraud and corruption and favoritism, on the one hand, and for robbing the people on the other. 'No, Colonel, Congress has no right to give charity. Individual members may give as much of their own money as they please, but they have no right to touch a dollar of the public money for that purpose. If twice as many houses had been burned in this county as in Georgetown, neither you nor any other member of Congress would have thought of appropriating a dollar for our relief. There are about two hundred and forty members of Congress. If they had shown their sympathy for the sufferers by contributing each one week's pay, it would have made over $13,000. There are plenty of wealthy men in and around Washington who could have given $20,000 without depriving themselves of even a luxury of life.' "The congressmen chose to keep their own money, which, if reports be true, some of them spend not very creditably; and the people about Washington, no doubt, applauded you for relieving them from the necessity of giving by giving what was not yours to give. The people have delegated to Congress, by the Constitution, the power to do certain things. To do these, it is authorized to collect and pay moneys, and for nothing else. Everything beyond this is usurpation, and a violation of the Constitution.'

" 'So you see, Colonel, you have violated the Constitution in what I consider a vital point. It is a precedent fraught with danger to the country, for when Congress once begins to stretch its power beyond the limits of the Constitution, there is no limit to it, and no security for the people. I have no doubt you acted honestly, but that does not make it any better, except as far as you are personally concerned, and you see that I cannot vote for you.'

"I tell you I felt streaked. I saw if I should have opposition, and this man should go to talking, he would set others to talking, and in that district I was a gone fawn-skin. I could not answer him, and the fact is, I was so fully convinced that he was right, I did not want to. But I must satisfy him, and I said to him:

" ‘Well, my friend, you hit the nail upon the head when you said I had not sense enough to understand the Constitution. I intended to be guided by it, and thought I had studied it fully. I have heard many speeches in Congress about the powers of Congress, but what you have said here at your plow has got more hard, sound sense in it than all the fine speeches I ever heard. If I had ever taken the view of it that you have, I would have put my head into the fire before I would have given that vote; and if you will forgive me and vote for me again, if I ever vote for another unconstitutional law I wish I may be shot.'

"He laughingly replied; 'Yes, Colonel, you have sworn to that once before, but I will trust you again upon one condition. You say that you are convinced that your vote was wrong. Your acknowledgment of it will do more good than beating you for it. If, as you go around the district, you will tell people about this vote, and that you are satisfied it was wrong, I will not only vote for you, but will do what I can to keep down opposition, and, perhaps, I may exert some little influence in that way.'

" ‘If I don't’, said I, 'I wish I may be shot; and to convince you that I am in earnest in what I say I will come back this way in a week or ten days, and if you will get up a gathering of the people, I will make a speech to them. Get up a barbecue, and I will pay for it.'

" ‘No, Colonel, we are not rich people in this section, but we have plenty of provisions to contribute for a barbecue, and some to spare for those who have none. The push of crops will be over in a few days, and we can then afford a day for a barbecue. This is Thursday; I will see to getting it up on Saturday week. Come to my house on Friday, and we will go together, and I promise you a very respectable crowd to see and hear you.’

" 'Well, I will be here. But one thing more before I say good-bye. I must know your name.’

" 'My name is Bunce.'

" 'Not Horatio Bunce?'

" 'Yes.’

" 'Well, Mr. Bunce, I never saw you before, though you say you have seen me, but I know you very well. I am glad I have met you, and very proud that I may hope to have you for my friend.'

"It was one of the luckiest hits of my life that I met him. He mingled but little with the public, but was widely known for his remarkable intelligence and incorruptible integrity, and for a heart brimful and running over with kindness and benevolence, which showed themselves not only in words but in acts. He was the oracle of the whole country around him, and his fame had extended far beyond the circle of his immediate acquaintance. Though I had never met him, before, I had heard much of him, and but for this meeting it is very likely I should have had opposition, and had been beaten. One thing is very certain, no man could now stand up in that district under such a vote.

"At the appointed time I was at his house, having told our conversation to every crowd I had met, and to every man I stayed all night with, and I found that it gave the people an interest and a confidence in me stronger than I had ever seen manifested before.

"Though I was considerably fatigued when I reached his house, and, under ordinary circumstances, should have gone early to bed, I kept him up until midnight, talking about the principles and affairs of government, and got more real, true knowledge of them than I had got all my life before.

"I have known and seen much of him since, for I respect him - no, that is not the word - I reverence and love him more than any living man, and I go to see him two or three times every year; and I will tell you, sir, if every one who professes to be a Christian lived and acted and enjoyed it as he does, the religion of Christ would take the world by storm.

"But to return to my story. The next morning we went to the barbecue, and, to my surprise, found about a thousand men there. I met a good many whom I had not known before, and they and my friend introduced me around until I had got pretty well acquainted - at least, they all knew me.

"In due time notice was given that I would speak to them. They gathered up around a stand that had been erected. I opened my speech by saying:

" ‘Fellow-citizens - I present myself before you today feeling like a new man. My eyes have lately been opened to truths which ignorance or prejudice, or both, had heretofore hidden from my view. I feel that I can today offer you the ability to render you more valuable service than I have ever been able to render before. I am here today more for the purpose of acknowledging my error than to seek your votes. That I should make this acknowledgment is due to myself as well as to you. Whether you will vote for me is a matter for your consideration only.’"

"I went on to tell them about the fire and my vote for the appropriation and then told them why I was satisfied it was wrong. I closed by saying:

" ‘And now, fellow-citizens, it remains only for me to tell you that the most of the speech you have listened to with so much interest was simply a repetition of the arguments by which your neighbor, Mr. Bunce, convinced me of my error.

" ‘It is the best speech I ever made in my life, but he is entitled to the

credit for it. And now I hope he is satisfied with his convert and that he will get up here and tell you so.'

"He came upon the stand and said:

" ‘Fellow-citizens - It affords me great pleasure to comply with the request of Colonel Crockett. I have always considered him a thoroughly honest man, and I am satisfied that he will faithfully perform all that he has promised you today.'

"He went down, and there went up from that crowd such a shout for Davy Crockett as his name never called forth before.'

"I am not much given to tears, but I was taken with a choking then and felt some big drops rolling down my cheeks. And I tell you now that the remembrance of those few words spoken by such a man, and the honest, hearty shout they produced, is worth more to me than all the honors I have received and all the reputation I have ever made, or ever shall make, as a member of Congress.'

"Now, sir," concluded Crockett, "you know why I made that speech yesterday.

"There is one thing now to which I will call your attention. You remember that I proposed to give a week's pay. There are in that House many very wealthy men - men who think nothing of spending a week's pay, or a dozen of them, for a dinner or a wine party when they have something to accomplish by it. Some of those same men made beautiful speeches upon the great debt of gratitude which the country owed the deceased--a debt which could not be paid by money--and the insignificance and worthlessness of money, particularly so insignificant a sum as $10,000, when weighed against the honor of the nation. Yet not one of them responded to my proposition. Money with them is nothing but trash when it is to come out of the people. But it is the one great thing for which most of them are striving, and many of them sacrifice honor, integrity, and justice to obtain it."

Patriotism

Not Yours To Give

Col. David Crockett

US Representative from Tennessee

Originally published in "The Life of Colonel David Crockett,"

by Edward Sylvester Ellis.

Col. David Crockett

US Representative from Tennessee

Originally published in "The Life of Colonel David Crockett,"

by Edward Sylvester Ellis.

One day in the House of Representatives a bill was taken up appropriating money for the benefit of a widow of a distinguished naval officer. Several beautiful speeches had been made in its support. The Speaker was just about to put the question when Crockett arose:

"Mr. Speaker--I have as much respect for the memory of the deceased, and as much sympathy for the sufferings of the living, if suffering there be, as any man in this House, but we must not permit our respect for the dead or our sympathy for a part of the living to lead us into an act of injustice to the balance of the living. I will not go into an argument to prove that Congress has not the power to appropriate this money as an act of charity. Every member upon this floor knows it. We have the right, as individuals, to give away as much of our own money as we please in charity; but as members of Congress we have no right so to appropriate a dollar of the public money. Some eloquent appeals have been made to us upon the ground that it is a debt due the deceased. Mr. Speaker, the deceased lived long after the close of the war; he was in office to the day of his death, and I have never heard that the government was in arrears to him.

"Every man in this House knows it is not a debt. We cannot, without the grossest corruption, appropriate this money as the payment of a debt. We have not the semblance of authority to appropriate it as charity. Mr. Speaker, I have said we have the right to give as much money of our own as we please. I am the poorest man on this floor. I cannot vote for this bill, but I will give one week's pay to the object, and if every member of Congress will do the same, it will amount to more than the bill asks."

He took his seat. Nobody replied. The bill was put upon its passage, and, instead of passing unanimously, as was generally supposed, and as, no doubt, it would, but for that speech, it received but few votes, and, of course, was lost.

Later, when asked by a friend why he had opposed the appropriation, Crockett gave this explanation:

"Several years ago I was one evening standing on the steps of the Capitol with some other members of Congress, when our attention was attracted by a great light over in Georgetown. It was evidently a large fire. We jumped into a hack and drove over as fast as we could. In spite of all that could be done, many houses were burned and many families made houseless, and, besides, some of them had lost all but the clothes they had on. The weather was very cold, and when I saw so many women and children suffering, I felt that something ought to be done for them. The next morning a bill was introduced appropriating $20,000 for their relief. We put aside all other business and rushed it through as soon as it could be done.

"The next summer, when it began to be time to think about election, I concluded I would take a scout around among the boys of my district. I had no opposition there, but, as the election was some time off, I did not know what might turn up. When riding one day in a part of my district in which I was more of a stranger than any other, I saw a man in a field plowing and coming toward the road. I gauged my gait so that we should meet as he came to the fence. As he came up, I spoke to the man. He replied politely, but, as I thought, rather coldly.

"I began: 'Well, friend, I am one of those unfortunate beings called

candidates, and---‘

"Yes I know you; you are Colonel Crockett. I have seen you once before, and voted for you the last time you were elected. I suppose you are out electioneering now, but you had better not waste your time or mine, I shall not vote for you again."

"This was a sockdolager...I begged him to tell me what was the matter.

" ’Well, Colonel, it is hardly worth-while to waste time or words upon it. I do not see how it can be mended, but you gave a vote last winter which shows that either you have not capacity to understand the Constitution, or that you are wanting in the honesty and firmness to be guided by it. In either case you are not the man to represent me. But I beg your pardon for expressing it in that way. I did not intend to avail myself of the privilege of the constituent to speak plainly to a candidate for the purpose of insulting or wounding you. I intend by it only to say that your understanding of the Constitution is very different from mine; and I will say to you what, but for my rudeness, I should not have said, that I believe you to be honest.

…But an understanding of the Constitution different from mine I cannot overlook, because the Constitution, to be worth anything, must be held sacred, and rigidly observed in all its provisions. The man who wields power and misinterprets it is the more dangerous the more honest he is.'

" 'I admit the truth of all you say, but there must be some mistake about it, for I do not remember that I gave any vote last winter upon any constitutional question.’

“ ‘No, Colonel, there’s no mistake. Though I live in the backwoods and seldom go from home, I take the papers from Washington and read very carefully all the proceedings of Congress. My papers say that last winter you voted for a bill to appropriate $20,000 to some sufferers by a fire in Georgetown. Is that true?’…But an understanding of the Constitution different from mine I cannot overlook, because the Constitution, to be worth anything, must be held sacred, and rigidly observed in all its provisions. The man who wields power and misinterprets it is the more dangerous the more honest he is.'

" 'I admit the truth of all you say, but there must be some mistake about it, for I do not remember that I gave any vote last winter upon any constitutional question.’

" ‘Well, my friend; I may as well own up. You have got me there. But certainly nobody will complain that a great and rich country like ours should give the insignificant sum of $20,000 to relieve its suffering women and children, particularly with a full and overflowing Treasury, and I am sure, if you had been there, you would have done just as I did.'

" ‘It is not the amount, Colonel, that I complain of; it is the principle. In the first place, the government ought to have in the Treasury no more than enough for its legitimate purposes. But that has nothing with the question. The power of collecting and disbursing money at pleasure is the most dangerous power that can be entrusted to man, particularly under our system of collecting revenue by a tariff, which reaches every man in the country, no matter how poor he may be, and the poorer he is the more he pays in proportion to his means. What is worse, it presses upon him without his knowledge where the weight centers, for there is not a man in the United States who can ever guess how much he pays to the government. So you see, that while you are contributing to relieve one, you are drawing it from thousands who are even worse off than he. If you had the right to give anything, the amount was simply a matter of discretion with you, and you had as much right to give $20,000,000 as $20,000. If you have the right to give to one, you have the right to give to all; and, as the Constitution neither defines charity nor stipulates the amount, you are at liberty to give to any and everything which you may believe, or profess to believe, is a charity, and to any amount you may think proper. You will very easily perceive what a wide door this would open for fraud and corruption and favoritism, on the one hand, and for robbing the people on the other. 'No, Colonel, Congress has no right to give charity. Individual members may give as much of their own money as they please, but they have no right to touch a dollar of the public money for that purpose. If twice as many houses had been burned in this county as in Georgetown, neither you nor any other member of Congress would have thought of appropriating a dollar for our relief. There are about two hundred and forty members of Congress. If they had shown their sympathy for the sufferers by contributing each one week's pay, it would have made over $13,000. There are plenty of wealthy men in and around Washington who could have given $20,000 without depriving themselves of even a luxury of life.' "The congressmen chose to keep their own money, which, if reports be true, some of them spend not very creditably; and the people about Washington, no doubt, applauded you for relieving them from the necessity of giving by giving what was not yours to give. The people have delegated to Congress, by the Constitution, the power to do certain things. To do these, it is authorized to collect and pay moneys, and for nothing else. Everything beyond this is usurpation, and a violation of the Constitution.'

" 'So you see, Colonel, you have violated the Constitution in what I consider a vital point. It is a precedent fraught with danger to the country, for when Congress once begins to stretch its power beyond the limits of the Constitution, there is no limit to it, and no security for the people. I have no doubt you acted honestly, but that does not make it any better, except as far as you are personally concerned, and you see that I cannot vote for you.'

"I tell you I felt streaked. I saw if I should have opposition, and this man should go to talking, he would set others to talking, and in that district I was a gone fawn-skin. I could not answer him, and the fact is, I was so fully convinced that he was right, I did not want to. But I must satisfy him, and I said to him:

" ‘Well, my friend, you hit the nail upon the head when you said I had not sense enough to understand the Constitution. I intended to be guided by it, and thought I had studied it fully. I have heard many speeches in Congress about the powers of Congress, but what you have said here at your plow has got more hard, sound sense in it than all the fine speeches I ever heard. If I had ever taken the view of it that you have, I would have put my head into the fire before I would have given that vote; and if you will forgive me and vote for me again, if I ever vote for another unconstitutional law I wish I may be shot.'

"He laughingly replied; 'Yes, Colonel, you have sworn to that once before, but I will trust you again upon one condition. You say that you are convinced that your vote was wrong. Your acknowledgment of it will do more good than beating you for it. If, as you go around the district, you will tell people about this vote, and that you are satisfied it was wrong, I will not only vote for you, but will do what I can to keep down opposition, and, perhaps, I may exert some little influence in that way.'

" ‘If I don't’, said I, 'I wish I may be shot; and to convince you that I am in earnest in what I say I will come back this way in a week or ten days, and if you will get up a gathering of the people, I will make a speech to them. Get up a barbecue, and I will pay for it.'

" ‘No, Colonel, we are not rich people in this section, but we have plenty of provisions to contribute for a barbecue, and some to spare for those who have none. The push of crops will be over in a few days, and we can then afford a day for a barbecue. This is Thursday; I will see to getting it up on Saturday week. Come to my house on Friday, and we will go together, and I promise you a very respectable crowd to see and hear you.’

" 'Well, I will be here. But one thing more before I say good-bye. I must know your name.’

" 'My name is Bunce.'

" 'Not Horatio Bunce?'

" 'Yes.’

" 'Well, Mr. Bunce, I never saw you before, though you say you have seen me, but I know you very well. I am glad I have met you, and very proud that I may hope to have you for my friend.'

"It was one of the luckiest hits of my life that I met him. He mingled but little with the public, but was widely known for his remarkable intelligence and incorruptible integrity, and for a heart brimful and running over with kindness and benevolence, which showed themselves not only in words but in acts. He was the oracle of the whole country around him, and his fame had extended far beyond the circle of his immediate acquaintance. Though I had never met him, before, I had heard much of him, and but for this meeting it is very likely I should have had opposition, and had been beaten. One thing is very certain, no man could now stand up in that district under such a vote.

"At the appointed time I was at his house, having told our conversation to every crowd I had met, and to every man I stayed all night with, and I found that it gave the people an interest and a confidence in me stronger than I had ever seen manifested before.

"Though I was considerably fatigued when I reached his house, and, under ordinary circumstances, should have gone early to bed, I kept him up until midnight, talking about the principles and affairs of government, and got more real, true knowledge of them than I had got all my life before.

"I have known and seen much of him since, for I respect him - no, that is not the word - I reverence and love him more than any living man, and I go to see him two or three times every year; and I will tell you, sir, if every one who professes to be a Christian lived and acted and enjoyed it as he does, the religion of Christ would take the world by storm.

"But to return to my story. The next morning we went to the barbecue, and, to my surprise, found about a thousand men there. I met a good many whom I had not known before, and they and my friend introduced me around until I had got pretty well acquainted - at least, they all knew me.

"In due time notice was given that I would speak to them. They gathered up around a stand that had been erected. I opened my speech by saying:

" ‘Fellow-citizens - I present myself before you today feeling like a new man. My eyes have lately been opened to truths which ignorance or prejudice, or both, had heretofore hidden from my view. I feel that I can today offer you the ability to render you more valuable service than I have ever been able to render before. I am here today more for the purpose of acknowledging my error than to seek your votes. That I should make this acknowledgment is due to myself as well as to you. Whether you will vote for me is a matter for your consideration only.’"

"I went on to tell them about the fire and my vote for the appropriation and then told them why I was satisfied it was wrong. I closed by saying:

" ‘And now, fellow-citizens, it remains only for me to tell you that the most of the speech you have listened to with so much interest was simply a repetition of the arguments by which your neighbor, Mr. Bunce, convinced me of my error.

" ‘It is the best speech I ever made in my life, but he is entitled to the

credit for it. And now I hope he is satisfied with his convert and that he will get up here and tell you so.'

"He came upon the stand and said:

" ‘Fellow-citizens - It affords me great pleasure to comply with the request of Colonel Crockett. I have always considered him a thoroughly honest man, and I am satisfied that he will faithfully perform all that he has promised you today.'

"He went down, and there went up from that crowd such a shout for Davy Crockett as his name never called forth before.'

"I am not much given to tears, but I was taken with a choking then and felt some big drops rolling down my cheeks. And I tell you now that the remembrance of those few words spoken by such a man, and the honest, hearty shout they produced, is worth more to me than all the honors I have received and all the reputation I have ever made, or ever shall make, as a member of Congress.'

"Now, sir," concluded Crockett, "you know why I made that speech yesterday.

"There is one thing now to which I will call your attention. You remember that I proposed to give a week's pay. There are in that House many very wealthy men - men who think nothing of spending a week's pay, or a dozen of them, for a dinner or a wine party when they have something to accomplish by it. Some of those same men made beautiful speeches upon the great debt of gratitude which the country owed the deceased--a debt which could not be paid by money--and the insignificance and worthlessness of money, particularly so insignificant a sum as $10,000, when weighed against the honor of the nation. Yet not one of them responded to my proposition. Money with them is nothing but trash when it is to come out of the people. But it is the one great thing for which most of them are striving, and many of them sacrifice honor, integrity, and justice to obtain it."

Wednesday, October 27, 2010

My Wordle

Well being that I have been quite lazy as of late and have been mostly copying other blogs I have found interesting. My friend over at The Crimson Cavalier posted his 100th post (kudos) and did this neat word cloud. I thought to go back and look over only the posts that I actually put keyboard to (so to speak) and this is what i ended up wtih:

Looking at the 3-5 largest words I think it adequately fits what I am most passionate about when I do decide to say something of my own.

Looking at the 3-5 largest words I think it adequately fits what I am most passionate about when I do decide to say something of my own.

Monday, October 18, 2010

Saturday, October 16, 2010

Creativity Abound!

For as much as I despise Apple products for their blatant attempt to become the mode of consumption for people rather than vehicles for productivity, I am admittedly wrong about Apple when it comes to creative types (artists, musicians, films). This performance was done solely on 4 Iphones plugged into a speaker. I'm speechless...

(UPDATE)

(UPDATE)

Friday, October 8, 2010

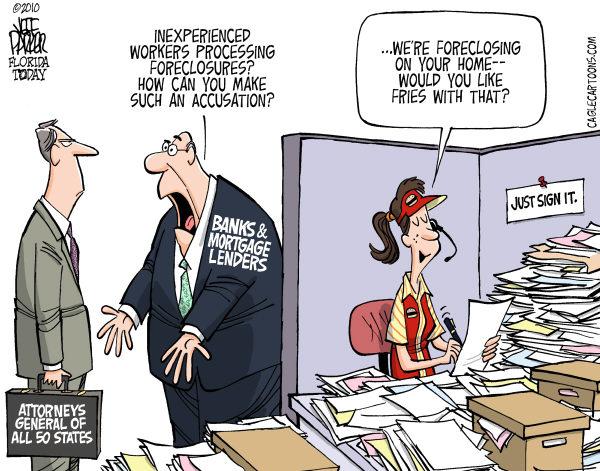

Much ado about nothing

Thank you Mr. President for making things clear

Presidential Memorandum--H.R. 3808

It is necessary to have further deliberations about the possible unintended impact of H.R. 3808, the "Interstate Recognition of Notarizations Act of 2010," on consumer protections, including those for mortgages, before the bill can be finalized. Accordingly, I am withholding my approval of this bill. (The Pocket Veto Case, 279 U.S. 655 (1929)).

The authors of this bill no doubt had the best intentions in mind when trying to remove impediments to interstate commerce. My Administration will work with them and other leaders in Congress to explore the best ways to achieve this goal going forward.

To leave no doubt that the bill is being vetoed, in addition to withholding my signature, I am returning H.R. 3808 to the Clerk of the House of Representatives, along with this Memorandum of Disapproval.

BARACK OBAMATHE WHITE HOUSE,

October 8, 2010.

So Furious!

Obama's back room politics strike again. Pandering to the big banks at the expense of the people.

INFURIATING LINK HERE

The author goes on to say that the law will actually become valid 10 days after it was put to Obama's desk for a signature.

Basically what this Law says is that Banks are allowed to notarize a document not in the presence of the signer. Which is complete and UTTER CRAP.

I AM FURIOUS!

INFURIATING LINK HERE

The word is out that Pres. Obama’s pocket veto of the Digital Robo-Signing Act was actually a trick. Sen. Harry Reid didn’t actually adjourn the U.S. Senate. The Senate has been kept in session by a little understood ruse and the bill will become law tonight at midnight without the President’s signature.The big banks will file suit after the election to have this bill declared to be law.Article I, Section 7 of the U.S. Constitution seems to support this view.Some drunken bankers were already bragging about this an some major news outlets, including Fox News have reported on this.

The author goes on to say that the law will actually become valid 10 days after it was put to Obama's desk for a signature.

Basically what this Law says is that Banks are allowed to notarize a document not in the presence of the signer. Which is complete and UTTER CRAP.

I AM FURIOUS!

Monday, October 4, 2010

Wednesday, September 29, 2010

Quote of the Day

"Do this. Don't do that. Stay back in line. Where's tax receipt? Fill out form. Let's see license. Submit six copies. Exit only. No left turn. No right turn. Queue up and pay fine. Take back and get stamped. Drop dead— but first get permit. "

-Robert Heinlein, The Moon Is a Harsh Mistress

-Robert Heinlein, The Moon Is a Harsh Mistress

Monday, September 27, 2010

Great Post From the Inner Workings Blog

Dave’s Top 10 Reasons the World Isn’t Coming to an End

Japanese-style stagnation, not economic collapse, is the most likely scenario for the US. Harrisburg, PA and Greece may go down the drain (and maybe even California and New York City and Illinois), but that’s not the end of the world. It’s just the end of them.

10) China’s controlled growth deceleration is doing reasonably well, according to Cantor Fitzgerald’s Asia strategist Uwe Parpart, my old Bank of America colleague.

9) China’s banks may be choking on bad loans, but China’s massive foreign exchange reserves can cover the problem out of petty cash and rounding error.

8) Southeast Asia continues to grow, with local stock exchanges up about 20% year to date.

7) India is doing well. Add up these first four items and half the world’s population is doing just fine.

6) Europe’s economic problem is less important than it seems because “Europe” is no longer the relevant entity. Germany is decoupling from France and the Club Med countries and shifting its focus to China and Russia.

5) Russia isn’t doing badly, thanks to 12 million foreign workers from Turkey and the Turkic former republics of the Soviet Union which have solved its labor shortage, while

4) Turkey is doing well exporting labor, construction services, and manufactures to Russia and the Arab world while acting as a hub for Russian oil.

3) Retirees around the world are hard pressed to find investments that yield enough to pay for their retirements, but it’s an ill wind that blows nobody good: the extremely low yields on long-term debt that generate a $3 trillion deficit for US state and local governments also benefit capital-intensive industries. It’s not a wash, but it’s not a washout, either.

2) Irresponsible as US monetary policy may be, there’s no alternative to the dollar, and there will not be for some time (I own a decent amount of gold in various forms in case I’m wrong about that) — so the US can get away with huge deficits for quite some time.

But the number one reason that the world isn’t coming to an end is –

1)Barack Obama! He’s cooked politically. He’s practically a lame duck. Gridlock in Washington will prevent this dreadful administration from doing any more damage. And that’s good news.

That said, it’s not the end of the world — it’s just the end of you, if you’re one of the 6 percent of the US population reaching retirement age during the next ten years, or if you’re a public employee counting on a pension, or run a small business. Life will go on in these United States, drearily. But don’t expect a great cataclysm to put you out of your misery.

The equity risk premium will remain stupidly high for reasons detailed in the link. But there’s no reason for stocks to crash, that is, for the equity risk premium to get even higher than it is now.

10) China’s controlled growth deceleration is doing reasonably well, according to Cantor Fitzgerald’s Asia strategist Uwe Parpart, my old Bank of America colleague.

9) China’s banks may be choking on bad loans, but China’s massive foreign exchange reserves can cover the problem out of petty cash and rounding error.

8) Southeast Asia continues to grow, with local stock exchanges up about 20% year to date.

7) India is doing well. Add up these first four items and half the world’s population is doing just fine.

6) Europe’s economic problem is less important than it seems because “Europe” is no longer the relevant entity. Germany is decoupling from France and the Club Med countries and shifting its focus to China and Russia.

5) Russia isn’t doing badly, thanks to 12 million foreign workers from Turkey and the Turkic former republics of the Soviet Union which have solved its labor shortage, while

4) Turkey is doing well exporting labor, construction services, and manufactures to Russia and the Arab world while acting as a hub for Russian oil.

3) Retirees around the world are hard pressed to find investments that yield enough to pay for their retirements, but it’s an ill wind that blows nobody good: the extremely low yields on long-term debt that generate a $3 trillion deficit for US state and local governments also benefit capital-intensive industries. It’s not a wash, but it’s not a washout, either.

2) Irresponsible as US monetary policy may be, there’s no alternative to the dollar, and there will not be for some time (I own a decent amount of gold in various forms in case I’m wrong about that) — so the US can get away with huge deficits for quite some time.

But the number one reason that the world isn’t coming to an end is –

1)Barack Obama! He’s cooked politically. He’s practically a lame duck. Gridlock in Washington will prevent this dreadful administration from doing any more damage. And that’s good news.

That said, it’s not the end of the world — it’s just the end of you, if you’re one of the 6 percent of the US population reaching retirement age during the next ten years, or if you’re a public employee counting on a pension, or run a small business. Life will go on in these United States, drearily. But don’t expect a great cataclysm to put you out of your misery.

The equity risk premium will remain stupidly high for reasons detailed in the link. But there’s no reason for stocks to crash, that is, for the equity risk premium to get even higher than it is now.

Thursday, September 23, 2010

Housing Has a Long way to go

From Zero Hedge:

On one end, you have the destruction left over from the extinction of US auto manufacturing. On the other end, you have PIMCO. And inbetween the two, there are 294 home markets, which make up the exponential curve of US real estate prices. It is not surprising that the non-normal distribution in home prices follows quite closely the Talebian extremistan distributions expected (even though the last word is an oxymoron in this context) out of modern day markets. We wonder which end of the curve the President has got his eyes focused most on these days for "excess efficiency" retention purposes.

According to the latest Coldwell Banker home listing report (link), the richest people in America reside in the following cities, which boast the following average home prices:

1.Newport Beach - $1,826,348

2.Palo Alto - $1,479,227

3.Rye - $1,325,500

4.San Francisco - $1,325,103

5.La Jolla - $1,210,300

6.Greenwich - $1,195,614

7.Wellesley - $1,080,458

8.Pasadena - $1,043,683

9.Honolulu - $1,026,821

10. Santa Barbara - $1,024,661

Alas for every market boasting an average home price over $1MM (ten of them), there are citis on the other end of the spectrum. And using the completely arbitrary cut off metric of $250,000, there are 145 markets whose homes cost less than that particular magic number, lef by the following:

1.Detroit - $68,007

2.Grayling - $84,625

3.Sioux City - $85,967

4.Cleveland - $87,240

5.Muncie - $100,314

6.Norfolk - $107,814

7.Kansas City - $112,449

8.Canton - $114,325

9.Port Huron - $116,267

10. Topeka - $116,343

At least Detroit is at the top of something. As is the broke state of California - with 6 of the 10 most expensive markets residing in the Golden State. We dread to think what will happen once the state's broke administrators realize how much wealth could be extracted from local housing if only they could collect a liiiittle bit of the net worth of each home (assuming said home is not already underwater on the debt it is pledged to).

On one end, you have the destruction left over from the extinction of US auto manufacturing. On the other end, you have PIMCO. And inbetween the two, there are 294 home markets, which make up the exponential curve of US real estate prices. It is not surprising that the non-normal distribution in home prices follows quite closely the Talebian extremistan distributions expected (even though the last word is an oxymoron in this context) out of modern day markets. We wonder which end of the curve the President has got his eyes focused most on these days for "excess efficiency" retention purposes.

According to the latest Coldwell Banker home listing report (link), the richest people in America reside in the following cities, which boast the following average home prices:

1.Newport Beach - $1,826,348

2.Palo Alto - $1,479,227

3.Rye - $1,325,500

4.San Francisco - $1,325,103

5.La Jolla - $1,210,300

6.Greenwich - $1,195,614

7.Wellesley - $1,080,458

8.Pasadena - $1,043,683

9.Honolulu - $1,026,821

10. Santa Barbara - $1,024,661

Alas for every market boasting an average home price over $1MM (ten of them), there are citis on the other end of the spectrum. And using the completely arbitrary cut off metric of $250,000, there are 145 markets whose homes cost less than that particular magic number, lef by the following:

1.Detroit - $68,007

2.Grayling - $84,625

3.Sioux City - $85,967

4.Cleveland - $87,240

5.Muncie - $100,314

6.Norfolk - $107,814

7.Kansas City - $112,449

8.Canton - $114,325

9.Port Huron - $116,267

10. Topeka - $116,343

At least Detroit is at the top of something. As is the broke state of California - with 6 of the 10 most expensive markets residing in the Golden State. We dread to think what will happen once the state's broke administrators realize how much wealth could be extracted from local housing if only they could collect a liiiittle bit of the net worth of each home (assuming said home is not already underwater on the debt it is pledged to).

Wednesday, September 22, 2010

Another Epically Good Post By Karl Denninger

From Market Ticker (The Folly Of Investing Today):

Investing is all about trying to determine a longer-term direction for the market such that risk and reward align in some meaningful way.

Yesterday, on Blogtalk, I stated that I was pulling all of my long-term investments that were market-related, and for an indeterminate time forward I would be only short-term trading this market.

That deserves an explanation, and toward this end, I would like to present the following 10 year weekly chart.

The regular "trace" is the S&P 500 price. The white trace is the 10 year Treasury yield as a comparative.

You need to pay attention to this.

"This time it's different" is often said.

It is almost always wrong, and believing in it will almost always make you broke.

Here's reality folks. Over the previous 10 years the TNX has never declined meaningfully without the S&P 500 following it, and declining to near or below it on a comparative basis.

The TNX almost always leads on declines too, sometimes by as much as six months.

Well, it's been six months.

In 2007, the TNX peaked in late June, after which it began a dive. The market peaked in the middle of October of that year at 1576. The decline essentially reached the comparative bottom.

Now the TNX has peaked the first week of April of this year, and is quite close to the March 2009 lows. Yet the S&P, after it took a swoon, has recovered.

Exactly as it did in 2007.

We all know what came next.

The same thing happened in 2000, when the market peaked and fell apart. Again, the TNX led. It in fact peaked almost exactly at the end of the year in 1999. Three months later "it" began.

The TNX move today, as I outlined in Ticks in real-time, broke a triangle formation that should have moved higher. That was a continuation pattern. Instead, it broke the wrong way - hard - even before The Fed announcement. After The Fed announcement the move was accentuated dramatically.

This is not a sign of "improvement" nor is it a sign to "buy stocks", as Cramer claimed today after the FOMC announcement. To the contrary. It is a strong signal to sell everything and get the hell away from the stock market. It is an indication that the market should, if it follows past precedent, decline by as much as 30%, and perhaps more.

The market usually leads the TNX when it bottoms and the market heads higher.

The TNX always leads the market when it declines.

The 2yr is at all time record low yields.

Lower than during the decline in 2008 and 2009.

This strongly implies that the March 2009 "666" low in the S&P 500 is NOT a "generational low", AND IT WILL IN FACT BE BREACHED.

The bond market is very, very rarely wrong folks. When it disagrees with equities you're a fool to believe the equities, unless of course you hate money.

This has always been true, and it will always be true.

The market is "betting" that Bernanke will come in with more "Quantitative Easing", or even better, that it can force Bernanke to implement more "Quantitative Easing." Japan in fact did this, and has continued to do so.

Where was the all-time high in the Nikkei 225, and where does it trade now? Did it ever get back to those highs?

No.

Does Japan have a massive foreign account deficit? No - they have a foreign account surplus. Their debt is owed to Japanese - not to foreigners, as ours is.

"Quantitative Easing" is a scam. It's yet another sop and fraud to allow the government to deficit spend "allegedly" without consequence. It covered $1 trillion of deficit spending the last time. If they do come in again all they will do is cover another $1 trillion in deficit spending by the government, while your actual disposable income in terms of goods and services will see yet more declines, just as occurred from 2000-2010.

That's all folks.

The "scam" part of it is that there is no way The Fed can ever reduce it's balance sheet once it does

this, because to do so the government will have to decrease spending by an equivalent amount to that "eased." It will never do so. Not voluntarily, anyway. Gold is moving higher on the bet that the attempt to "allow" continued government spending will fail and ultimately the government will be forced to default (either literally or through massive unsterilized money printing that destroys the currency.) I don't think that will prove correct - I think our foreign creditors will pull our credit card first. But that's what Gold is saying, and if Gold is right, then America as a nation is finished, and our government will eventually dissolve either into outright tyranny or civil war and you will be THROWING your gold at people to defend yourself.

The only way The Fed can "fix" the market and economy in the intermediate term is to raise rates. That is, remove liquidity and force rates higher. Doing so will cause the TNX to rise along with the rest of the yield curve.

It will also shut down the Federal Government's deficit spending binge immediately as they will not be able to fund both that binge and the (higher) interest payments on the debt.

Bernanke is not going to do it.

Not now, not ever, unless he is forced by external events, and I believe eventually he WILL be.

Unlike Japan we cannot play this game as they did, simply because of our foreign account deficits. Japan got away with it for as long as they did for that reason, but even their capacity to do so is becoming strained.

The simple truth is that Bernanke can't pull liquidity at the present time because the government is spending all of its tax receipts paying for entitlements.

Even if the economy "recovers" he still can't do it because doing so means that interest expense would more than double, and the government doesn't have the money now and won't even under a rosy economic recovery scenario.

This is an environment in which it makes sense to own stocks as investments?

The hell it does.

This is a classic "death spiral" situation and equity valuations are in a severe bubble as a consequence of all the government "cheese", despite "appearing" to be "cheap."

Bernanke has bricked himself into the outhouse and he knows it. Thus, all the "soft threats" to "quantitative ease" and all the screaming from both the left and right for yet more of it - both sides know exactly what sort of box they're trapped in, and it's a box of their own design.

Oh sure, there can be short-term pops in the market. They might even last months. There could even be parabolic moves upward. The Nikkei has had several of them.

But you cannot invest in them.

You can trade them, and if you have the time and patience to do so in a dispassionate fashion then have at it, but you cannot invest in equities, nor can you buy any coupon (bonds) with any sort of meaningful duration.

If you do, you will ultimately be destroyed.

Those pension funds and other investors who are "reaching for yield" and "reaching for risk" at the present time are making the biggest mistake of their lives. It is inevitable that this strategy will fail and when it does what you formerly thought was "safe" - whether it be your pension, your Social Security, your Medicare, your kid's prepaid college education - all of it will be gone.

This preoccupation with Bernanke's folly is not only unhealthy, it is certifiably insane.

The TNX does not lie folks.

It has not in the past - not even when "Easy Al" was running the joint and handing out money like candy. Nor has it this time, with Bernanke doing the exact same thing Easy Al was doing.

Policies haven't changed and until they do neither will market relationships.

Act as you deem best, but ignore the bond market at your considerable peril.

It is rarely wrong.

Investing is all about trying to determine a longer-term direction for the market such that risk and reward align in some meaningful way.

Yesterday, on Blogtalk, I stated that I was pulling all of my long-term investments that were market-related, and for an indeterminate time forward I would be only short-term trading this market.

That deserves an explanation, and toward this end, I would like to present the following 10 year weekly chart.

The regular "trace" is the S&P 500 price. The white trace is the 10 year Treasury yield as a comparative.

You need to pay attention to this.

"This time it's different" is often said.

It is almost always wrong, and believing in it will almost always make you broke.

Here's reality folks. Over the previous 10 years the TNX has never declined meaningfully without the S&P 500 following it, and declining to near or below it on a comparative basis.

The TNX almost always leads on declines too, sometimes by as much as six months.

Well, it's been six months.

In 2007, the TNX peaked in late June, after which it began a dive. The market peaked in the middle of October of that year at 1576. The decline essentially reached the comparative bottom.

Now the TNX has peaked the first week of April of this year, and is quite close to the March 2009 lows. Yet the S&P, after it took a swoon, has recovered.

Exactly as it did in 2007.

We all know what came next.

The same thing happened in 2000, when the market peaked and fell apart. Again, the TNX led. It in fact peaked almost exactly at the end of the year in 1999. Three months later "it" began.

The TNX move today, as I outlined in Ticks in real-time, broke a triangle formation that should have moved higher. That was a continuation pattern. Instead, it broke the wrong way - hard - even before The Fed announcement. After The Fed announcement the move was accentuated dramatically.

This is not a sign of "improvement" nor is it a sign to "buy stocks", as Cramer claimed today after the FOMC announcement. To the contrary. It is a strong signal to sell everything and get the hell away from the stock market. It is an indication that the market should, if it follows past precedent, decline by as much as 30%, and perhaps more.

The market usually leads the TNX when it bottoms and the market heads higher.

The TNX always leads the market when it declines.

The 2yr is at all time record low yields.

Lower than during the decline in 2008 and 2009.

This strongly implies that the March 2009 "666" low in the S&P 500 is NOT a "generational low", AND IT WILL IN FACT BE BREACHED.

The bond market is very, very rarely wrong folks. When it disagrees with equities you're a fool to believe the equities, unless of course you hate money.

This has always been true, and it will always be true.

The market is "betting" that Bernanke will come in with more "Quantitative Easing", or even better, that it can force Bernanke to implement more "Quantitative Easing." Japan in fact did this, and has continued to do so.

Where was the all-time high in the Nikkei 225, and where does it trade now? Did it ever get back to those highs?

No.

Does Japan have a massive foreign account deficit? No - they have a foreign account surplus. Their debt is owed to Japanese - not to foreigners, as ours is.

"Quantitative Easing" is a scam. It's yet another sop and fraud to allow the government to deficit spend "allegedly" without consequence. It covered $1 trillion of deficit spending the last time. If they do come in again all they will do is cover another $1 trillion in deficit spending by the government, while your actual disposable income in terms of goods and services will see yet more declines, just as occurred from 2000-2010.

That's all folks.

The "scam" part of it is that there is no way The Fed can ever reduce it's balance sheet once it does

this, because to do so the government will have to decrease spending by an equivalent amount to that "eased." It will never do so. Not voluntarily, anyway. Gold is moving higher on the bet that the attempt to "allow" continued government spending will fail and ultimately the government will be forced to default (either literally or through massive unsterilized money printing that destroys the currency.) I don't think that will prove correct - I think our foreign creditors will pull our credit card first. But that's what Gold is saying, and if Gold is right, then America as a nation is finished, and our government will eventually dissolve either into outright tyranny or civil war and you will be THROWING your gold at people to defend yourself.

The only way The Fed can "fix" the market and economy in the intermediate term is to raise rates. That is, remove liquidity and force rates higher. Doing so will cause the TNX to rise along with the rest of the yield curve.

It will also shut down the Federal Government's deficit spending binge immediately as they will not be able to fund both that binge and the (higher) interest payments on the debt.

Bernanke is not going to do it.

Not now, not ever, unless he is forced by external events, and I believe eventually he WILL be.

Unlike Japan we cannot play this game as they did, simply because of our foreign account deficits. Japan got away with it for as long as they did for that reason, but even their capacity to do so is becoming strained.

The simple truth is that Bernanke can't pull liquidity at the present time because the government is spending all of its tax receipts paying for entitlements.

Even if the economy "recovers" he still can't do it because doing so means that interest expense would more than double, and the government doesn't have the money now and won't even under a rosy economic recovery scenario.

This is an environment in which it makes sense to own stocks as investments?

The hell it does.

This is a classic "death spiral" situation and equity valuations are in a severe bubble as a consequence of all the government "cheese", despite "appearing" to be "cheap."

Bernanke has bricked himself into the outhouse and he knows it. Thus, all the "soft threats" to "quantitative ease" and all the screaming from both the left and right for yet more of it - both sides know exactly what sort of box they're trapped in, and it's a box of their own design.

Oh sure, there can be short-term pops in the market. They might even last months. There could even be parabolic moves upward. The Nikkei has had several of them.

But you cannot invest in them.

You can trade them, and if you have the time and patience to do so in a dispassionate fashion then have at it, but you cannot invest in equities, nor can you buy any coupon (bonds) with any sort of meaningful duration.

If you do, you will ultimately be destroyed.

Those pension funds and other investors who are "reaching for yield" and "reaching for risk" at the present time are making the biggest mistake of their lives. It is inevitable that this strategy will fail and when it does what you formerly thought was "safe" - whether it be your pension, your Social Security, your Medicare, your kid's prepaid college education - all of it will be gone.

This preoccupation with Bernanke's folly is not only unhealthy, it is certifiably insane.

The TNX does not lie folks.

It has not in the past - not even when "Easy Al" was running the joint and handing out money like candy. Nor has it this time, with Bernanke doing the exact same thing Easy Al was doing.

Policies haven't changed and until they do neither will market relationships.

Act as you deem best, but ignore the bond market at your considerable peril.

It is rarely wrong.

Tuesday, September 21, 2010

The Biggest Issue of 2010, In One Chart

If you were asked to produce a single chart illustrating the biggest single political issue in America today, what would it look like?

We're taking on that challenge today. Here's what we came up with:

In this chart, where we've graphed the trajectory of the total spending of the federal government with respect to the median household income in the U.S. for the years from 1967 through 2009, we see that the U.S. federal government's spending today has decoupled from the primary source of income that is required to sustain it.

In this chart, where we've graphed the trajectory of the total spending of the federal government with respect to the median household income in the U.S. for the years from 1967 through 2009, we see that the U.S. federal government's spending today has decoupled from the primary source of income that is required to sustain it.

Worse, it has literally "gone vertical" during the last two years.

In mathematical terms, that's the sort of thing you see when you divide any number by zero. Applied to the chart above, that means that the relationship between the change in total government spending and the typical income earned by an American household from year-to-year is now "undefined."

In practical terms, that means government spending has become completely disconnected from the ability of the typical American household to support it. And until this skyrocketing spending growth is arrested and reversed, we suspect that government spending has become disconnected from the ability of any American household to support it.

U.S. Census. Table H-5. Race and Hispanic Origin of Householder -- Households by Median and Mean Income (1967-2009).

We're taking on that challenge today. Here's what we came up with:

In this chart, where we've graphed the trajectory of the total spending of the federal government with respect to the median household income in the U.S. for the years from 1967 through 2009, we see that the U.S. federal government's spending today has decoupled from the primary source of income that is required to sustain it. Worse, it has literally "gone vertical" during the last two years.

In mathematical terms, that's the sort of thing you see when you divide any number by zero. Applied to the chart above, that means that the relationship between the change in total government spending and the typical income earned by an American household from year-to-year is now "undefined."

In practical terms, that means government spending has become completely disconnected from the ability of the typical American household to support it. And until this skyrocketing spending growth is arrested and reversed, we suspect that government spending has become disconnected from the ability of any American household to support it.

Data Sources

White House, Office of Management and Budget. Historical Tables, Budget of the U.S. Government, Fiscal Year 2011. Table 3.1 - Outlays by Superfunction and Function: 1940-2015.U.S. Census. Table H-5. Race and Hispanic Origin of Householder -- Households by Median and Mean Income (1967-2009).

Wednesday, September 15, 2010

Fundamental Investors Should Fear Inflation, Not Deflation

Just a great concise view on the prospects of inflation in the future.

Fundamental Investors Should Fear Inflation, Not Deflation

Submitted by Rich Toscano and John Simon on September 13, 2010 - 11:05am.

Summary- While continued low inflation or another bout of price deflation are both possible, there are several factors -- none of which require an economic recovery -- that could prevent deflation or even cause inflation to surprise to the upside.

- In the event that deflation does take place, we believe it will be met with a powerfully inflationary policy response. As a result, any foray into deflation will likely be relatively brief.

- Any deflation-fighting policies enacted will further strengthen the already robust, fundamentally-driven case for a significant eventual loss of dollar purchasing power against things that people need to buy.

- Rather than speculating on inherently unpredictable short-term events, we prefer to own a diversified basket of investments that stand to benefit from our high-confidence, fundamentally supportable long-term forecasts.

In this article we employ the standard usage of the terms "inflation" and "deflation" as protracted changes in the aggregate price level of consumer goods and services. Some analysts describe changes to the money supply, system credit, or asset prices as inflation or deflation. These are all important factors that exert an impact on general consumer price levels, as we described in a previous article on the mechanisms of deflation, but we think it only confuses matters to use the same term to describe multiple phenomena. For this reason, and because this article concerns itself primarily with the purchasing power of US dollars, we will stick with the most commonly accepted definition of inflation and deflation as changes to consumer prices.

Neither Deflation nor Continued Low Inflation Are Certainties

Our monetary and political system is so biased towards inflation that it took an unprecedented private sector credit collapse -- along with the attendant financial market panic, severe economic downturn, and energy price crash -- in order to cause just six months of CPI deflation back in 2008.

The implosion phase of private sector deleveraging is already behind us. We do believe that a credit bubble still exists, but that it has moved to the government debt sector. As we will discuss below, a crisis in government debt would not be deflationary in the way that the private sector credit collapse was. So it is far from assured that there will be another wave of deflationary force sufficiently massive enough to overcome our systematic inflation bias and push us into outright deflation.

Meanwhile, there are several potential circumstances that could overcome the current economic weakness and continued (though much slower than late 2008) debt deleveraging that are both currently keeping inflation low:

-- More quantitative easing. At the last Federal Reserve policy meeting, it was ordained that the proceeds from maturing mortgage-backed securities and bonds (purchased during the prior round of quantitative easing) would be rolled over into purchases of US Treasuries. This policy move put to bed any talk of an "exit plan" for the Fed's wildly stimulative monetary policy. It also sent a signal that the Fed is willing to use quantitative easing ("QE" -- a fancy term for the direct creation of new money in order to buy assets) not just as a crisis measure but as an ongoing policy tool.

This latest move takes place at a time when inflation is still positive and the stimulus-driven recovery, while feeble and getting weaker, is still somewhat intact. More quantitative easing could well take place if the current lull continues, but in our opinion, QE2 would be almost a sure thing if the economy were to take another leg down or the CPI were to start dropping.

The first round of QE appeared to help put a fairly quick end to CPI deflation, but there are too many factors involved to be certain of causality. Still, logic dictates that if QE causes new money to be created and circulated, prices of at least some items will go up more than they would have. In addition to increasing the amount of money being circulated, quantitative easing could also cause a loss of confidence in the dollar -- also a potentially inflationary outcome.

The money created by QE1 tended to just sit in reserves, so it did not get into general circulation in sufficient amounts to create much overall CPI inflation (although one could argue that it was sufficient to forestall further deflation). But that need not be the case with QE2. If the Fed monetizes US Treasuries, then the newly created money being supplied to the government can be disbursed to consumers via fiscal stimulus measures (see next section). If that doesn't work, the Fed could monetize other assets or make purchases from non-banks in order to get the new money into wider circulation. While not specifically quantitative easing, the Fed could further widen monetary circulation by directly granting loans to private parties. The options available to the Fed are many, and the Fed has both stated and demonstrated that it is willing to use non-standard policies to boost inflation.

Another round of QE seems likely if the current stagnation continues, almost assured if we actually dip into deflation again, and could very well head off deflation or even cause a surge in inflation. Just based on the possibility of further QE alone, we'd be very hesitant to declare future low inflation or deflation a sure thing.

-- More fiscal stimulus. Unemployment is stubbornly high, voters are unhappy with the weak economy, and high-profile economists are screaming that another Great Depression is guaranteed without huge further stimulative efforts. Under these circumstances, it's not unrealistic to expect more fiscal stimulus. If we were to dip into actual deflation again, the case for increased stimulus would become stronger still.

Scattered mentions of austerity pop up here and there, but in most cases we believe that this is just empty electioneering. The reality is that few politicians are willing to be the ones to force meaningful belt-tightening, especially should they find themselves in the midst of a deflation scare or serious economic downturn.

More stimulus is likely at some point, but given the widespread public bitterness towards Wall Street, future spending will probably not be aimed at propping up the financial industry. Instead, the next round of stimulus is likely to target jobs, wages, and general spending within the economy. Such spending programs would be more likely to stoke inflation than the prior bank-bailout stimulus.

-- A falling dollar. There is a widespread belief that inflation can't take place in the absence of rising wages, but this is not the case. A decline in the foreign exchange value of the dollar could drive up import and commodity prices for Americans, causing a loss of dollar purchasing power even in an environment of stagnant wages.

Currency-driven inflations against a backdrop of (often extreme) economic weakness have been quite common historically, so we are puzzled as to why this possibility is completely ignored by most analysts.

A currency-driven inflation would likely not consist of an across-the-board increase in prices. Prices of items affected by exchange rates, such as food, energy, and imported goods would rise even as items that weren't affected as much by exchange rates -- notably, housing -- stagnated or declined. The price indices, averaging out all items as they do, might not even look like they were rising much, but this would feel very much like inflation as people would find that their money was losing purchasing power against the things that they needed most.

A sufficiently large dollar decline could additionally undermine confidence in the currency, leading people to exchange their dollars for more reliable stores of value and driving prices up further.

-- A US government debt crisis. We believe that a crisis of confidence in US government debt at some point is a high-probability event. The reason, in very brief, is that the US has amassed enough foreign debt that there is no politically feasible way to pay it off in real terms. Eventually, we believe, our creditors will come to understand this reality and will begin to price it into our debt.

A crisis in Treasury debt would look very different from the deflationary private-sector credit bust of 2008. Back then, Treasuries and the dollar were the so-called "safe havens" to which panicky investors fled. If the US government's solvency came into question, that safe haven status would be lost and investors would likely be clamoring to get out of the very same assets that they piled into in 2008. A resulting flight out of US dollars could have the inflationary effects described in the "falling dollar" section above.

The inflationary potential would likely be exacerbated by the belief -- probably correct -- that the Fed would monetize Treasuries in order to keep a lid on rates, thus substantially increasing the money supply.

The timing of a crisis in US sovereign debt will be driven more by crowd psychology than by anything else, so we don't think it's possible to predict ahead of time when it will take place. But we believe that something like this will occur, that it is likely the next big crisis that our nation will have to face -- and that it has the potential to be highly inflationary.